While consumer confidence has slipped back a little in recent months, Savills’ experts, in the “UK Shopping Center and High Street Bulletin, Q 4/2014,” continue to believe that 2015 will be the first year of a robust consumer recovery across the country. The combination of low inflation and further delays in the inevitable rise in the Bank of England’s base interest rate will make the average household in the United Kingdom feel richer, and the latest employment numbers should also add to the general positive feeling among consumers. While some coverage of the slowing rate of inflation has focused on how shoppers might see this as a reason to defer spending, we believe that the fact that the main drivers of this low level of inflation are fuel and food limits the prospect of waiting for a better deal next week.

The main lurking horrors for this year are probably around a potentially inconclusive election result or an EU referendum. Both would have a negative impact on consumer confidence, though the former would be shorter term than the latter. Ultimately, the key retail economy theme for 2015 is the return of real earnings growth, and this can only be good news for retailers and landlords alike.

THE RETAIL OCCUPATIONAL MARKET

It is clear from Christmas trading statements that retailers in the United Kingdom generally had a better time over this key trading period than they did in 2013 and 2014. Average like-for-like (LFL) sales growth for those who have reported to date was 6.9%, an improvement on the 4.8% reported last year. Of course, the picture was not entirely rosy, with negative LFL sales reported by food retailers, in particular. Furthermore, while there were relatively few statements on margins, it is clear that they remained under pressure and those who over-embraced discounting around Black Friday suffered particularly hard. Indeed, given the general negativity of reporting around this US import, 2015 may well see a lot less noise about this event.

Looking ahead to the rest of 2015, Savills expects it to be a significantly better year for retailers, with real earnings growth now back in positive territory and the fall in fuel prices in particular likely to be viewed as a tax cut by the country’s consumers. While retailers will continue to run a forensic eye over their store portfolios, Savills’ experts expect that this year will see a net increase in store numbers, with the key battlegrounds being larger stores in prime towns and pitches, as well as infill in recovering secondary markets.

Dividing the year in halves, the first half of 2015 will see the incentives being offered to retailers eroding, while the second half of the year will actually deliver some real headline rental growth in the most sought-after locations. The best locations may well not be the most obvious “prime” markets. Indeed, towns with higher rents (with Zone A rents in excess of £250/sq ft) may well show lower growth than the recently re-based markets where retailers can make a more credible story for margin improvement.

Another new trend for 2015 will be the beginnings of a recovery in development activity, particularly in terms of the refurbishment and expansion of secondary malls. Savills expects to see new projects starting in a number of locations where the land value is sufficiently low on the owners’ books to justify investment. In many cases, these projects will be jump-started by a more mixed-use focus to combine leisure and residential with the existing retail offer. 2015 will undoubtedly be a turning point in the cycle for retailers in the United Kingdom, and while we expect to see further store rationalization, there is demand for units that are being released by food retailers and others. Most importantly, demand will be national and not overly focused on a few prime towns and pitches in London and the Southeast.

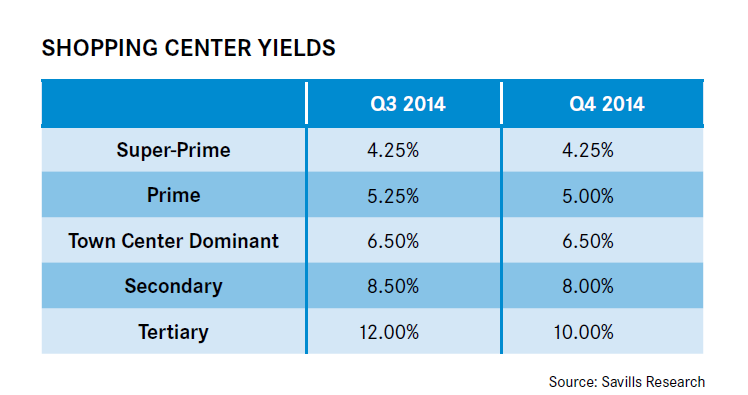

SHOPPING CENTER INVESTMENT

The shopping center investment market witnessed a surge in activity in 2014. A total of 100 centers transacted in 2014, representing a capital value of £6.05 billion. This is a 32% increase on the £4.58 billion traded in 2013. There are also currently 21 shopping centers under offer accounting for around £930 million and twengy on the market accounting for an additional £900 million.

NOTABLE DEALS IN THE FOURTH QUARTER OF 2014:

- The asset swap of Princesshay in Exeter from Land Securities to TIAA Henderson for £128 million and Buchanan Galleries Glasgow from TIAA Henderson to Land Securities for £137.5 million.

- The acquisition of the Mander Center in Wolverhampton by Benson Elliot off Delancey/RBS for £58 million.

- The acquisition of a 50% stake in Highcross in Leicester by Hammerson off clients of LaSalle Investment Management for £216 million.

- The acquisition by Chris Lazari of Brunswick Shopping Center in London off clients of LaSalle Investment Management for £135 million.

- The acquisition of Fremlin Walk Maidstone by M and G off L and G for £110 million.

- HSBC’s acquisition of The Centre in Livingston off Land Securities for £224 million.

The fourth quarter of last year saw intense activity in the shopping center market, with increased investor activity and demand for the sector from all quarters. One of the defining reasons why Savills believes the market will continue to surge forward in the short to medium term is the fact that we are in unprecedented times from an investor appetite perspective. The experts have never witnessed a market where all sectors of the investor spectrum are seeking to deploy equity at the same point alongside the debt markets. This is primarily because the sovereign wealth funds – and global institutions hadn’t started to deploy equity around the globe until relatively recently.

From a market perspective, Savills believes 2015 will see a slowdown in the large loan portfolio sales from banks. This has been a key feature of the market over the last 24 months. The company’s experts believe that they will begin to see many of the large opportunity funds start to work out some of their positions – indeed this has already started to happen. Portfolio sales will continue to be a market theme. In 2014, high profile portfolios such as Project Swallowtail, The Tiger Portfolio, and, to a lesser extent, Carbon attracted unprecedented levels of interest over the summer months as they enabled end purchasers to acquire numerous assets and attract strong banking terms.

As yields on the more secondary assets harden, there we will see a number of the pan European opportunity funds look to other less mature markets to reach their return criteria. To be competitive, return hurdles will have to be lowered to “core” levels of around 10% to be able to compete.

Institutional investors for the most part continue to enjoy cash inflows. Savills has also witnessed a huge influx of new buyers to the market. Indeed, in 2014, there were a total of 64 parties involved in such deals. This included both equity providers and asset managers. In 2009, just 18 equity providers/asset managers were involved in transactions.