The total sales of the top 1,000 online shops in 2013 were a cool €30 billion, an increase of 4.1%. This is only about a quarter of the growth rate achieved in 2012 (16.1%). “Despite the significantly slower growth of e-commerce,the boom is not over yet. It is merely showing the signs of a market that is maturing over the years,” comments Lars Hofacker, Director of the Department of E-Commerce at EHI, referring to the study “E-Commerce Market Germany 2014” by EHI and Statista.

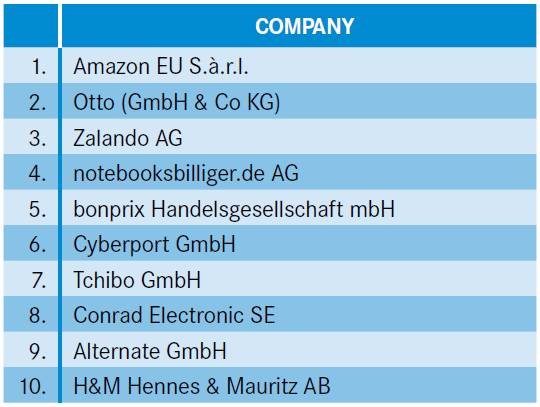

THE TOP 10 GERMAN E-COMMERCE RETAILERS (BY TURNOVER)

Another change: concentration has increased. Over a third (37.1% compared to 32.3% the year before) of the turnover in the e-commerce market stems from just 10 companies (see chart). The top 100 stores account for almost two-thirds and the top 500 for 86% of total sales. The ranking is topped by amazon.de and otto.de, followed for the first time by zalando.de. The generalists represent the largest share of the overall market – almost 40%. They are followed in second place by the “clothing, textiles, and shoes” segment (18.6%), ahead of “computers, consumer electronics, and mobile phone accessories” at 12.8%. The market shares of all the other segments are below four percent.

SHOPPING FROM ANYWHERE

More and more online shops are following the trends toward smart phone accessibility. The growth rate for mobile sites with store functions is a remarkable 95.9%. The proportion rose to 38.4% compared with last year’s 19.6%. Shops increasingly offer apps with shopping functions as well. Android solutions (15.9%) have now almost caught up to iPhone apps (16.7%). Facebook is here to stay as a sales promoter: 88.9% of online shops use the social network and most of them are happy with their 10,000 to 50,000 “likes.”

ABOUT THE STUDY. In its sixth edition, the study is now the standard bearer for the market. The Excel file provided includes details on each of the 1,000 top-selling online stores and offers a unique opportunity to conduct detailed analyses of the market, for example by product segment on over 170 store features. Information on traffic, apps, payment options, shop and product reviews, delivery methods, social media, sales channels, and shop and contact details are just a few examples of the information it contains.

The study is available in EHI’s webshop for download: http://www.ehi-shop.de/en/ecommerce

IMAGE: EHI