By Caroline Milne and Zsolt Toth

These are strong–but not surprising–words from Antonio Guterres, UN Secretary-General, at the opening ceremony of COP in Glasgow on November 1st. Representing 37% of the global share of CO2 emissions and 36% of total energy spend, buildings represent an enormous opportunity to help reverse climate change. Every sector, every individual, must take swift action to reverse their contribution to climate change and change the course of history our planet is taking. Retail real estate is not exempt from this journey.

In October, 2021 BPIE (Buildings Performance Institute Europe) published a vision and a step-wise roadmapprecisely to ensure that retail real estate would not be left behind on the global journey to reach 2050 net zero carbon emissions, in line with the Paris Agreement. The roadmap is the result of over one year of engagement with 14 retail European and global property developers, investors and managers.

No lack of willpower to reach net zero carbon

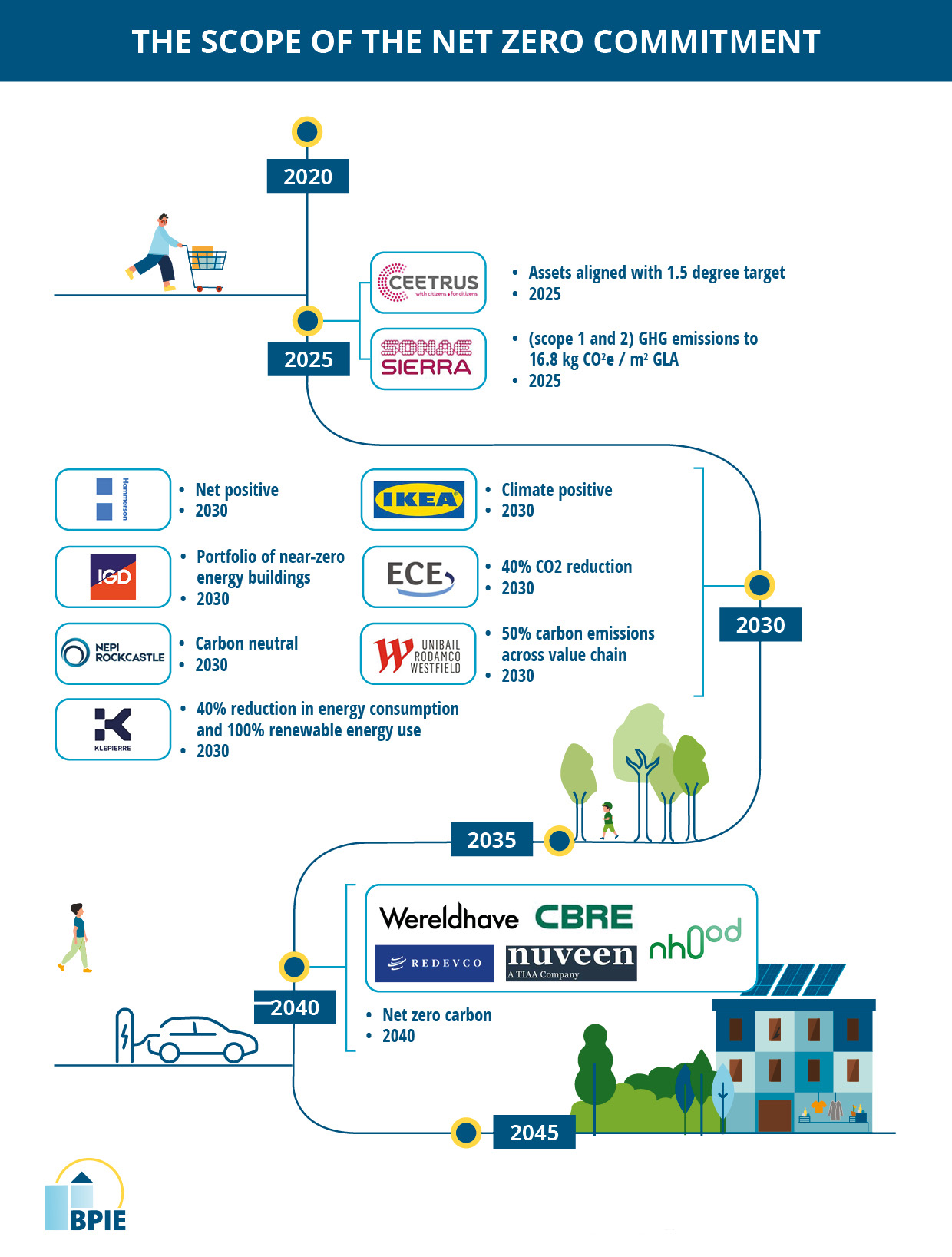

Throughout over a year of engagement with leading figures representing the retail real estate sector, one thing became abundantly clear: there is no shortage of will power and awareness to decarbonize. But what’s lacking is a clear roadmap on how to get there and how policymakers can make this journey easier for the RRE sector. The figure below provides an overview of a number of current RRE pledges, highlighting the growing ambition level in the sector.

And that’s not surprising: achieving net zero carbon is far from straightforward. Net zero and carbon neutral(among others) have become catchphrases–ones that we hear being thrown around all too easily. There remains a great deal of uncertainty around what it actually means, or what the industry-wide route to net zero actually is or should be.

On the path to carbon neutrality, efforts to contribute to Paris Agreement alignment need to be articulated, developed, and scaled across the sector–and done so rapidly. As part of the climate alignment efforts, there are plenty of opportunities for the sector to create sustainable places and contribute to maintaining the social fabric.

Zero carbon is good business

The challenge to climate neutral should be seen as a challenge to improve a business’s bottom line. Done well, sustainability and climate-driven initiatives–improving energy and material efficiency, extending renewable capacities, rethinking supply chains and even transforming business models–have the potential to create competitive advantage, attract preferential financing and investment, attract better retail tenants, improve cash flows, and drive innovation and revenue growth.

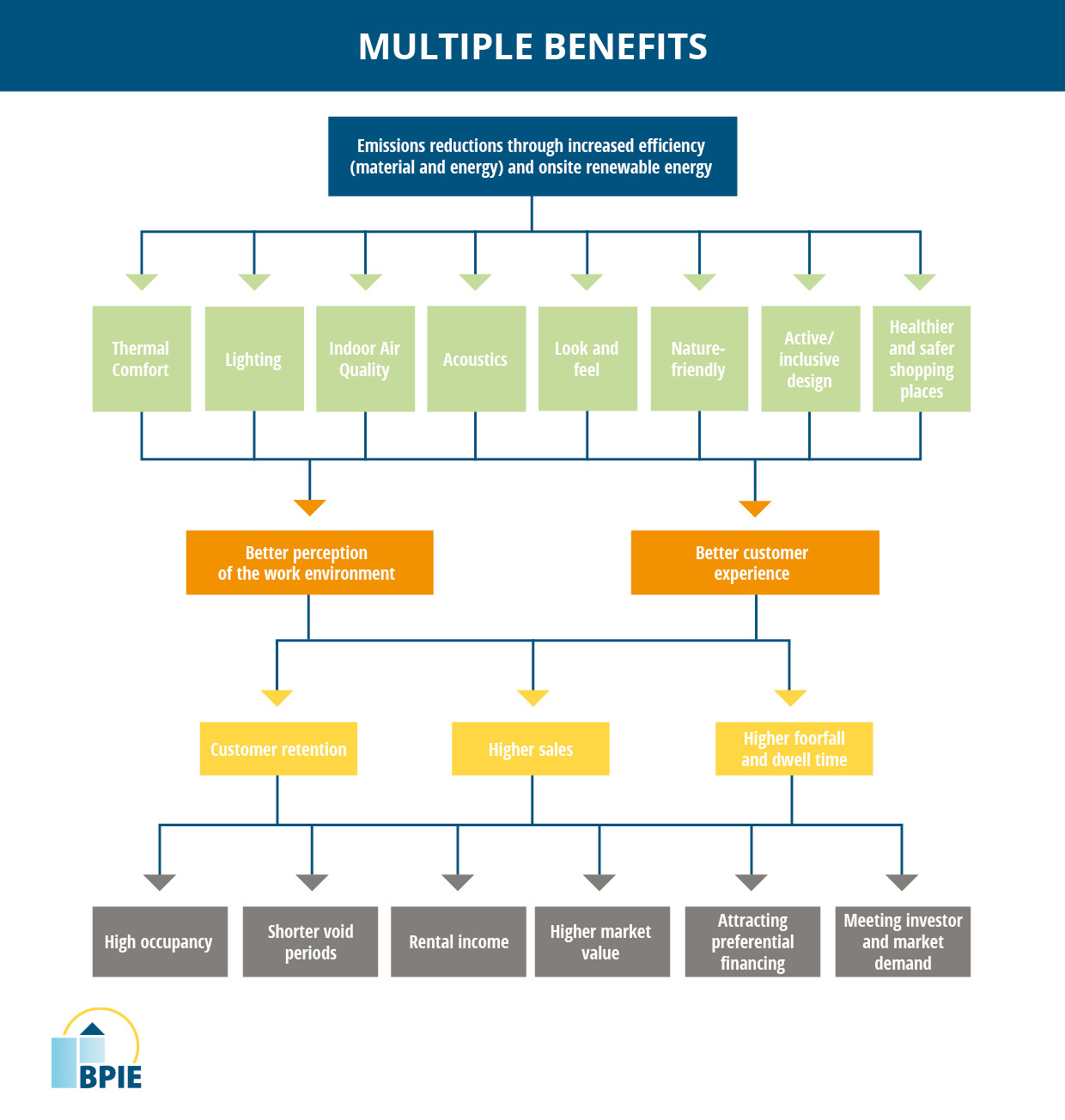

Investing in low-carbon solutions and improving building performance often have multiple wider associated benefits. Key non-energy/carbon gains, such as an improved indoor climate, can affect staff, customers, and consumer experience. Greener, healthier retail stores–those which typically have good levels of daylight, fresh air and greenery–are not only more attractive to consumers but could also improve footfall and sales. These quality aspects are all the more relevant in the context of the recovery from the current health crisis. Delivering the ambition of a zero carbon RRE sector will entail realizing the full extent of these gains.

The sector will need a better understanding of how low-carbon initiatives can be translated into different types of business value, and how they can measure the return on sustainability-driven investments in a more guided and considered way. Linking low carbon with wider sustainability considerations and benefits, such as sustainable store design and the health of staff and customers, can help to accelerate and deepen the integration of carbon-related initiatives into business strategy and operations. These can also provide a common language to engage both landlord and retailer in improving environmental performance in retail spaces.

Strategic, coordinated efforts needed

The retail real estate sector cannot go it alone. There are many challenges policymakers and industry must address, requiring unprecedented levels of collaboration. Executing any kind of net zero strategy over the long-term requires a supportive policy framework. Currently, EU policymakers are preparing a number of legislative revisions as part of the Renovation Wave strategy, notably the Energy Performance of Buildings Directive (EPBD), which is expected in December 2021. This process will provide ample opportunity for retail real estate to engage with policy and ensure a supportive policy framework now and in years to come.

Decarbonization of the RRE sector cannot, and should not, be looked at in isolation from the much wider built environment value chain. Rather, it must be positioned relative to decarbonization activity within interrelated sectors and industries such as construction, energy and transport. There are many interdependencies, overlaps and common themes among the connected sectors and individual mitigation measures.

Developing a zero-carbon roadmap for the RRE sector requires acknowledgement and understanding of these interdependencies between sectors and markets. Without close collaboration and coordination with other sectors, there is a real risk of displacing carbon between industries.

Roles and responsibilities by 2025

BPIE’s roadmap explains what the property sector, policymakers, commercial tenants, the construction sector, and financial institutions must do by 2025, 2030, and 2040. Looking just at the short-term, there are many things all the key stakeholders within the industry can and should do by 2025.

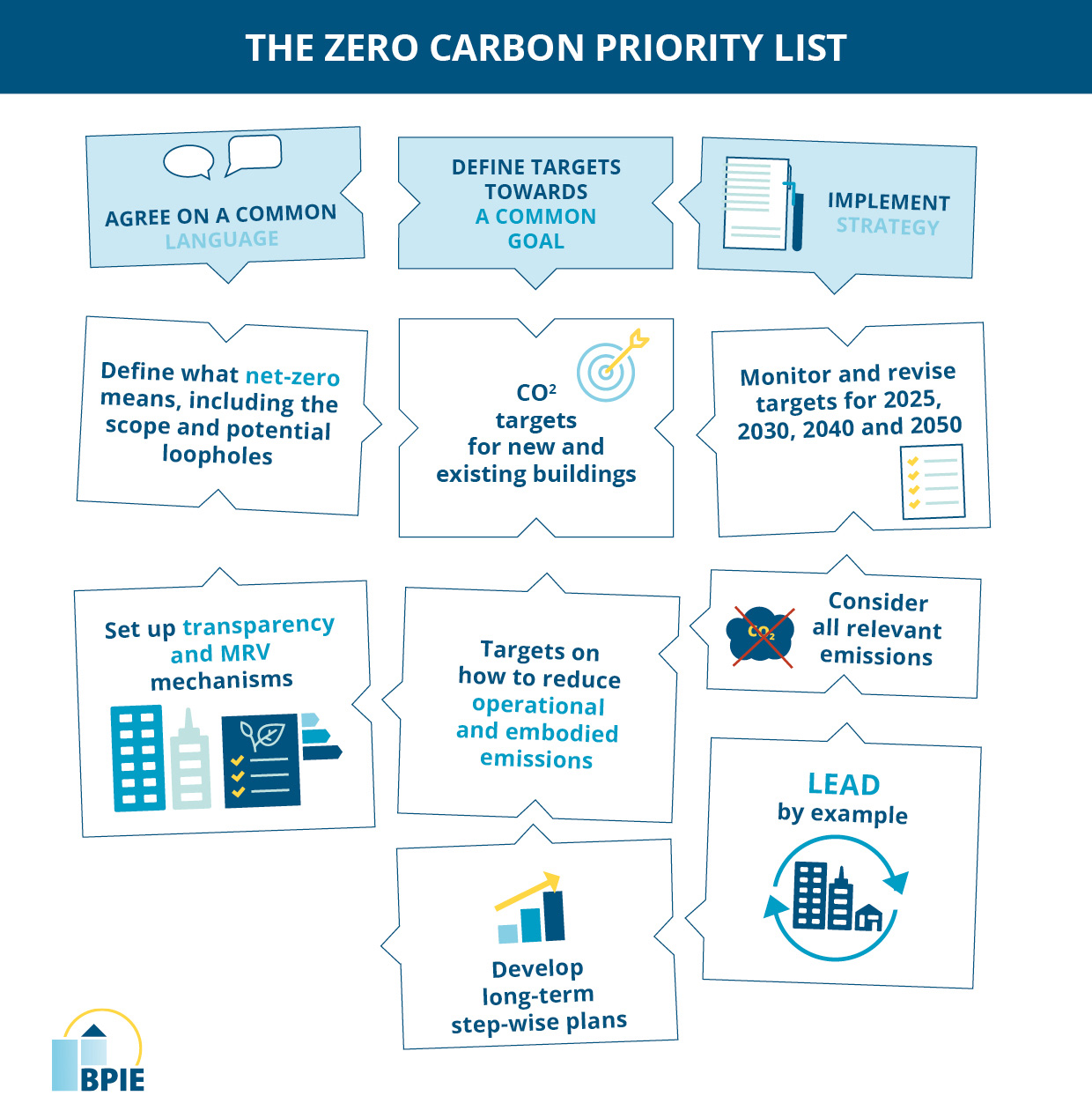

For example, the retail real estate sector needs to define short-, medium-, and long-term science-based targets to reduce the carbon footprint of assets and portfolios, as well as provide a plausible climate strategy based on scenario and carbon pricing modelling in line with IPCC’s 1.5°C degrees. Additionally, the sector must work on the harmonization and consistency of KPIs, metrics and assessment frameworks, make the carbon related risks and benefits more tangible by robust and detailed analysis of the impacts of intervention strategies and retrofit solutions, and improve the collection, disclosure and sharing of GHG data.

Integrating energy, carbon, and financial performance datasets to develop more strategic foresight and communicate the impacts of different retrofit measures across the RRE sector is also vital. And that’s just the start.

On their part, by 2025 policymakers should further tighten building codes, including whole life carbon limits, introduce policy roadmaps to a carbon neutral building stock, including specific requirements for different sectors, and mandate lifecycle assessments for new constructions and major renovations to identify ways to minimize all carbon emissions.

The introduction of mandatory minimum carbon performance standards to oblige the worst-performing buildings to be renovated can be facilitated through an updated and improved energy performance certificate (EPC) framework that discloses carbon emissions in a reliable way. Finally, a robust measurement, reporting and compliance mechanism to monitor and guarantee carbon reduction in the building sector needs to be put in place.

Institutional investors must commit to shift investments in RRE portfolios to net zero carbon by 2040 and incentivize investments in energy efficiency and low-carbon solutions, while the EU and national banks should support the sector’s roadmap to net zero through targeted subsidies and loans.

Retailers and tenants need to integrate the carbon performance of the building into business strategies, thereby increasing demand for high-performing and low-carbon buildings and implement green lease clauses with building owners. On a more human level, they have the responsibility to train personnel to change behavior and implement a low-carbon workplace, and develop strategies to nudge customers towards low-carbon behavior.

Finally, by 2025 the construction sector and real estate service providers should define short-, medium- and long-term science-based targets, set up new ways to collaborate across the construction value chain and develop strategies to meet the increasing demand for low-carbon solutions.

The power of technologies must be harnessed by developing digital solutions to measure and track emissions over the whole lifecycle and new business models based on serial/modular renovation techniques, including industrial-scale manufacturing and innovative solutions (such as robotics or 3D printing). In the next few years, it will also be important to develop and demand information about the environmental impact of construction products, as well as invest in training to enable the transition to net zero carbon.

Aligning the sector with a zero-carbon goal cannot follow a static and fixed pathway. The strategy will have to be regularly reviewed and updated to ensure that goals and thresholds are as robust and relevant as possible and reflect the state of the markets and progress on climate outcomes. But one thing is for sure as BPIE’s vision document communicates: the industry is ready to play its part in meeting the climate challenge and delivering a net zero carbon future.

It is now in the hands of all industry players to work together to make sure that this strategy is used, regularly reviewed, and communicated to policymakers.