By Klaus Striebich

In numerous articles, posts, webinars, commissioned expert opinions, and other elaborations one is able to read and listen to why owners of commercial real estate can still “insist” on payment of rent despite officially mandated closures during the period of Covid-19/coronavirus. However, an equal number of explanations have also be given as to why tenants of such retail properties should have exactly the opposing “rights”.

Are the multitude of differing and conflicting statements of any help? Has a battle against and by means of paragraphs broken out, instead of against the real problem? A little more knowledge and understanding of the other side might prove helpful, paired with a genuine desire for mutual solidarity as well as the foresight to comprehend that success in the future will only be achieved by working together, and that short-term individual perspectives will likely exacerbate the real problem.

This report serves as an attempt to illustrate the situation faced by retail tenants in retail properties. The current situation regarding the retail sector will be presented in three phases: “pre-”, “mid-”, and “post-” the period encompassing the coronavirus pandemic.

Pre-coronavirus

There is no denying that the situation with regard to brick-and-mortar retail was somewhat problematic even prior to the sudden outbreak of the virus. Noticeable changes in consumer behavior, coupled with the need for retailers to adopt a multi-channel concept, the technical race to catch up in terms of digitalization, etc., have clearly revealed a number of deficits, problems, and challenges. However, the fact that even the somewhat weaker market participants at the time were, nevertheless, welcome buyers of existing or newly developed rental space in the real estate industry cannot be refuted. Where possible, they were to conclude long-term leases at rental rates that were in line with market levels.

Was that indicative of the rather short-term thinking and behavior of both owners and landlords, ignorance of the situation, naivety, or even negligence? ”Honi soit qui mal y pense“(Shame on him who thinks this evil) – motto of the British Order of the Garter, probably coined by King Edward III. (1312-1377). From a retail perspective, a normal month can be depicted as shown in the table below.

This is a simplified model, which, of course, can also show variations depending on the company and its dependencies. A “normal” month serves as the starting point, generating a sales volume of 100 (or percent, if preferable) and a cost of goods to be sold of 50, which logically results in a margin of 50. That margin is then used to cover the costs incurred in the course of that month, e.g., personnel, rental costs, depreciation and interest, marketing, and other expenses. A profit is desirable, as is the case in the example (of 5). In the given example, the cash flow of the retailer is comprised of the generated surplus of 5 and the non-discharged Depreciation Allowance / Interest item of 5, which amounts to a total of 10.

An unforeseen drop in sales of -6, for example, would then result in a monthly loss of -1 (expected sales of 100 – sales drop of 6 = actual sales of 94 – cost of goods sold of 50 = margin of 44 – costs of 45 = loss of -1). In fact, the cost of goods sold is (normally) not reduced, because the goods have already been purchased and are in stock, thereby rendering them payable. The running costs were incurred as planned, because the actual sales are not shown until the end of the month.

The purpose of this simple calculation example is to highlight the fragility of the retail sector, whose development can vary from day to day. The retail sector is, of course, responsible for reacting to such changes and taking measures to ensure that profits are made across the board, which is what makes subsequent future investments possible.

Mid-coronavirus

Slight fluctuations in sales can usually be managed, as long as there are days or months in which additional sales can be generated (also in order to sell goods that have accumulated in the warehouse).

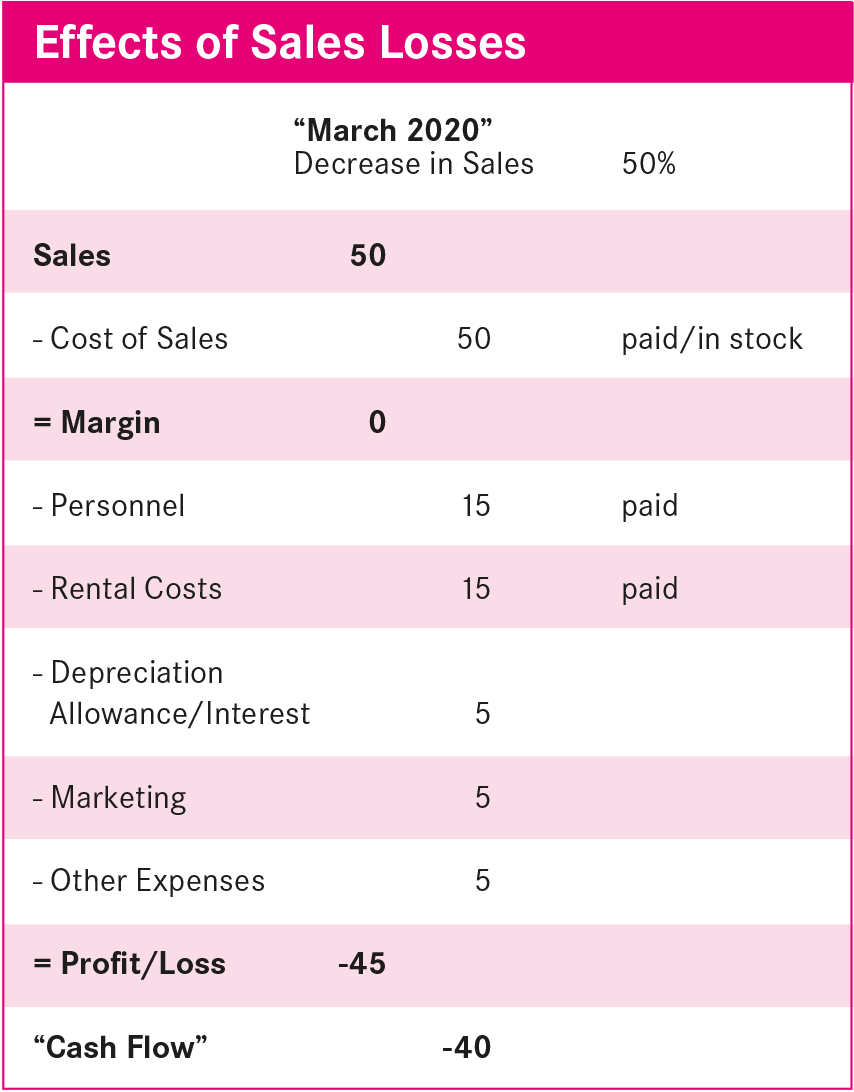

The primary problem caused by the lockdown in March was, effectively, the extremely high drop in sales of approximately 50%, which was neither planned nor foreseeable. The originally planned profit of 5 resulted in a loss of -45 (which is the equivalent of 9 months of planned profit).

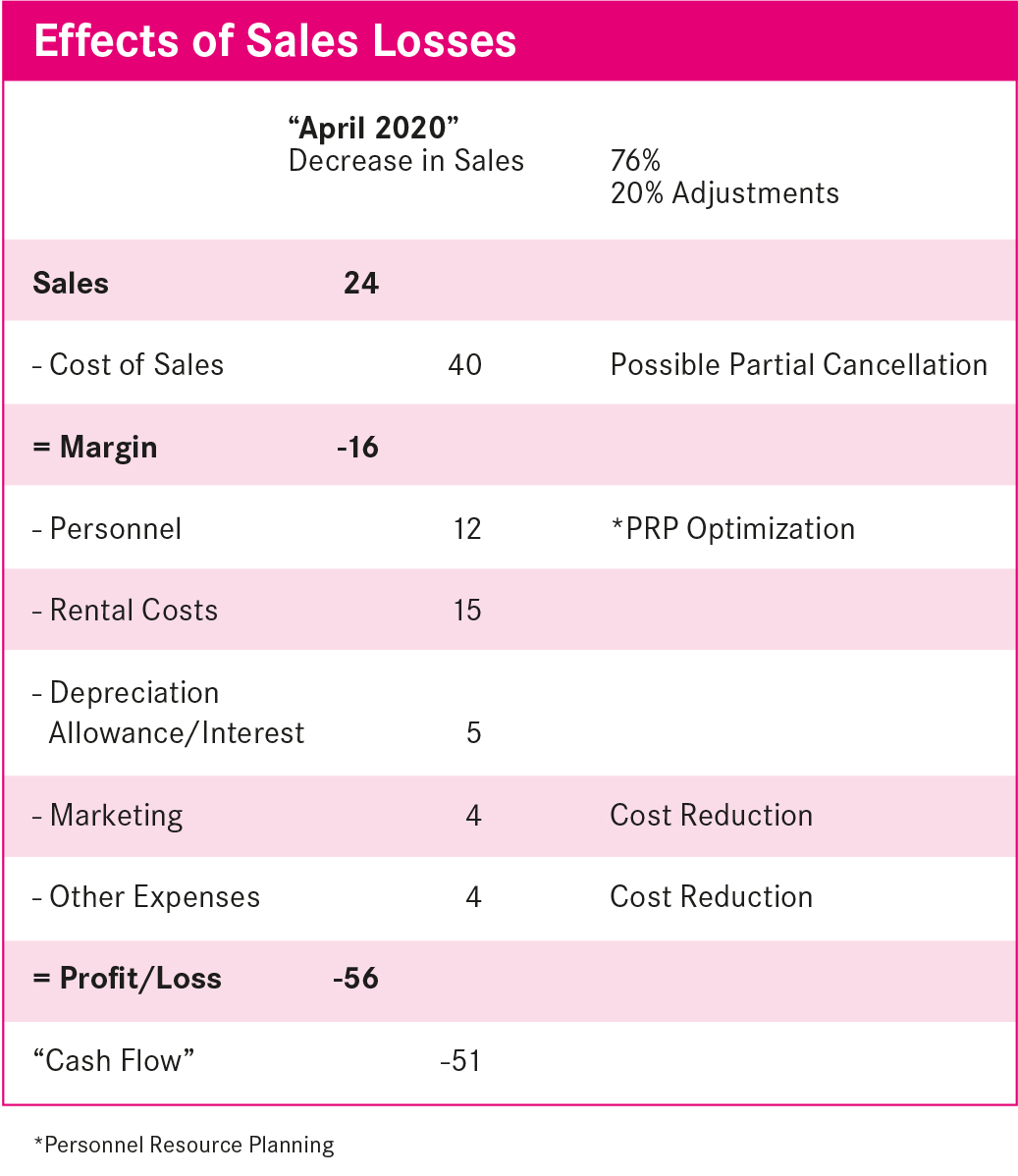

The following month of April, which saw the complete closure of brick-and-mortar stores, exacerbated the problem to a monthly loss of (only) -56, based on the -76% drop in sales reported in the textile industry, for example. Retailers had already reacted or had been forced to react to the situation by making adjustments to the supply of goods (if possible), as well as to personnel and other costs. If the rent for the month of April was not paid, the loss is only reduced to -41 (which is equivalent to 8 months of planned profit).

In simple terms, the months of March and April will result in a loss of at least -50 (10 months x 5 – losses in March and April of -101) from a planned annual profit of 60 (12 months x 5). How long a retail company can depend on its own resources or on the support of banks and owners for its survival varies from case to case. Insolvency or a lack of funds can be brought on relatively quickly, thereby rendering “the end” economically foreseeable. All parties involved should be aware of such consequences. Rapid reaction by the responsible retail managers, primarily through the creation and maintenance of liquidity, is both necessary and essential for survival.

Such action includes the use of all aid packages offered by the government, such as the use of short-time working allowances (who is the work done by in such cases?), credit guarantees (which at some point have to be paid back), deferrals (which were granted by law for a period of three months), or other suspensions of payments. The cash flow consideration shall be left to the reader, because loan commitments and payments usually take four to six weeks to be processed, and short-time work allowances have to be pre-financed or are “topped up” in order to secure the workforce. The figures speak for themselves.

Companies that are prepared for crises have quickly been able to make use of their online offers and media presence and have been able to compensate for one thing or another; however, even those companies are far from able to compensate for the lost offline sales.

Post-coronavirus

During the month of May, the opportunity to open locations and generate sales has been re-established. Retailers have to plan anew and should, for example, make the following assumptions (again, in very simplified terms): During the month, a drop in sales will level off at around -33 (depending on the number of opening days in the month and the corresponding purchasing behavior of the customers), cost adjustments and measures will be implemented in the amount of -33% for goods (because these should actually be available on site) and personnel; all measures will only be changed by -20%. There will be a deficit in the result as well as in the cash flow.

With the knowledge gained from the three previous coronavirus months, the retailer’s planned result for this year has probably changed from +60 to: -63.4 (9 months x 5 – losses for the months of March to May), which is effectively representative of a reversal of all previous signs (viewed somewhat cynically).

An extremely positive outlook could involve the retailer being able to reach the planned sales level of 100 again (from the month of June), but due to the high stock of goods and tougher market conditions, being required to operate with discounts of 10% on average in addition to slightly increased marketing efforts:

The looming danger of upcoming discount battles as a result of accumulated inventory and the lack of a catch-up effect in customer purchasing will, in turn, make it impossible to make a profit in terms of the operating result. The current state of affairs can only be eased in small steps – if at all. The implications for the year-end result can be deduced and calculated.

So much for the situation in the retail sector.

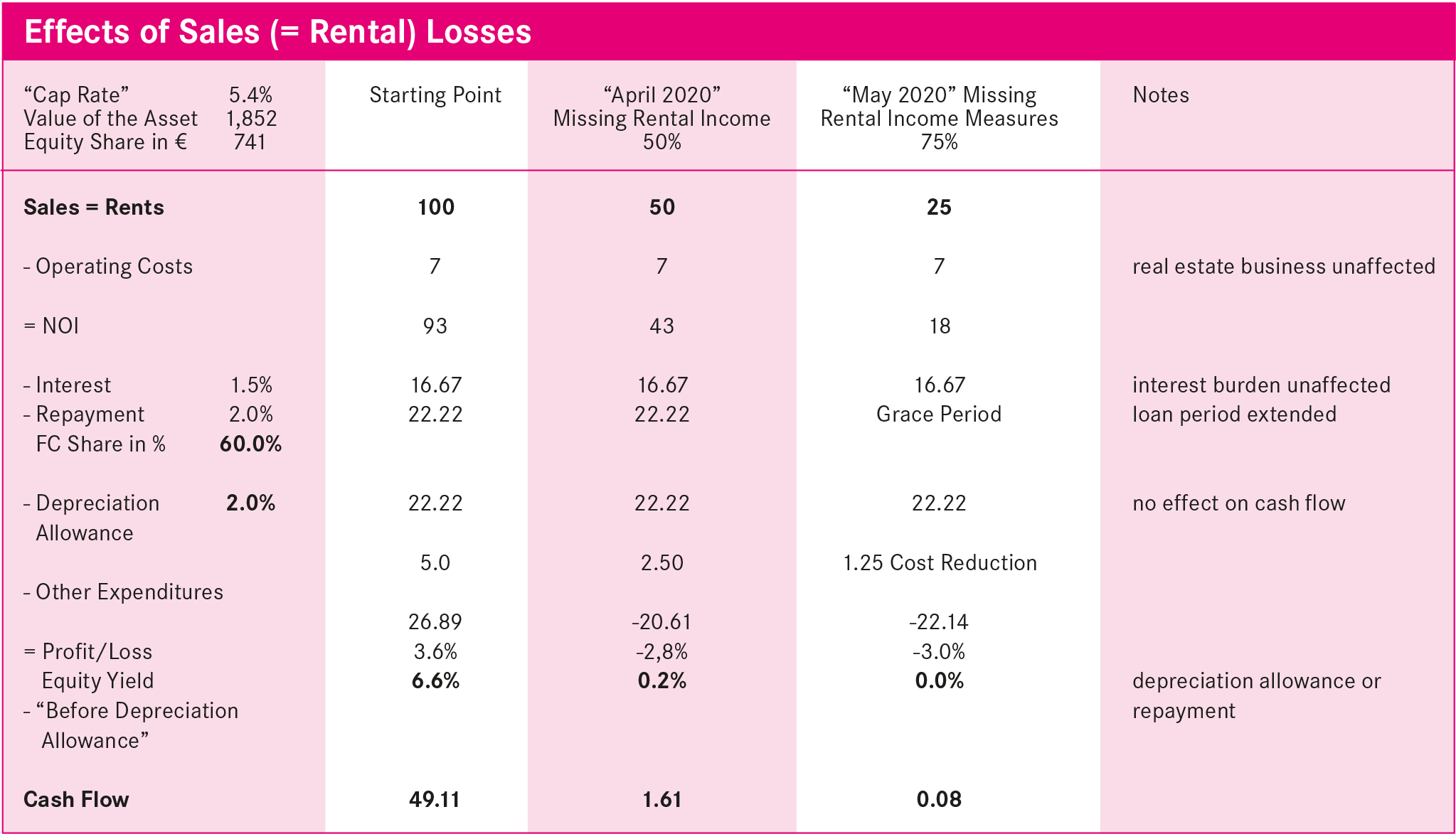

Property owners and landlords are, naturally, commercial enterprises as well and have obligations and payments to make. A (simplified, quite positive) presentation of a commercial property under the assumption of various premises, which can, of course, differ from other cases, illustrates this point:

To explain the sample calculation: The sales generated by the property owners are the rents. In this example, the starting point is 100. Operating costs for the property (non-distributable service charges, etc.) amount to 7. Regarding interest, 16.6 is to be paid (with a debt ratio of 60% and an interest rate of 1.5%), and an average rate of 2% is to be assumed for repayment, which results in a repayment amount of 22.2. With the additional “other costs” of 5, a cash flow of 49 is generated, a surplus of 26.9 is achieved using a factoring rate of 2%, which then results in a return on equity of 6.6% or 3.6%.

A 50% loss of rental income (equivalent to a decline in turnover) naturally results in a huge slump in surplus and thus a loss – as can be seen in the “March 2020” column. More importantly, however, the cash flow remains positive. In times such as these, property landlords also have to react in an entrepreneurial manner. Possible measures include adjusting the other costs, if necessary, and discussions with banks to extend repayment periods, if expedient. The operating costs and interest on the borrowed capital remain unchanged in the calculation. In the “May 2020” column, the calculation is backwards, and one could remain cash flow neutral using this calculation approach as well as the measures implemented if rents were reduced by up to 75%. At this point, the discussion regarding suspended service charge payments or yield promises for investors has been deliberately left aside.

Up to this point, neither party would achieve a good result, but it may allow for long-term survival. If the tenant, despite various measures and efforts, does not succeed in continuing to operate successfully and has to (forcibly) give up the location, the landlord will be faced with the issue of subsequent use and the assessment of a possible rental rate.

Another (simplified) calculation model compares the situation involving a reduction in rent with a possible long-term reduction in rent:

The reduction of two months’ rent in one year is counterbalanced by the threat of a possible decrease in rents of less than 1%. The costs associated with a change of tenant and loss of rental income have not been included for the sake of simplicity. The extent to which the valuation of the properties will change in the event of a complete loss of market participants on the tenant market and a reduced number of requests for space (and generally not suitable for one’s own property) can be assessed by each individual (or entered into discussion with one’s property valuer).

Conclusion

Sober calculation, threat, or assistance? Every case and every situation presents itself in an individual and different way. There are many different parameters that have to be considered and weighed by both parties. The aforementioned calculations only serve as examples and are not “blueprints”. They merely serve as illustrations. In addition, there are numerous other aspects, parameters, and, most importantly, ideas regarding possible further cooperation.

It is absolutely essential that we closely consider the situation of the respective other party, to communicate and act in a sensible manner. This should, ideally, be done in an active, cooperative, and constructive manner and with a view to long-term, joint success, which will enable us to overcome even such – hopefully short-term – difficult times.

Closing Remark

The complete omission of legal and contractual discussions or so-called formal requirements of any kind was entirely deliberate.