Statement of the publisher, Reinhard Winiwarter: The topic of retail parks with their current developments and benefits is being widely discussed, especially after the pandemic-related acceleration of trends and the need to adapt quickly. This asset class is proving to be of high value across Europe. ACROSS has published the in-depth Online Special “Retail Parks: Everybody’s Darling?” recently: you can subscribe here to get up to date.

To further underline the rising importance, we happily present more insight with a study by RegioPlan, explaining the market distribution of retail parks in Europe.

To get up to date on this topic, read the ACROSS Online Special “Retail Parks: Everybody’s Darling?” and subscribe here:

During times of coronavirus crisis, retail parks have become the focus of interest within the retail real estate asset classes. Conservative and non-retail-related investors in particular find a comparably safe investment in these assets, while shopping malls stay attractive for even less conservative investors. Especially larger-scaled, local supply oriented retail parks with a strong food retailer as anchor are most sought after.

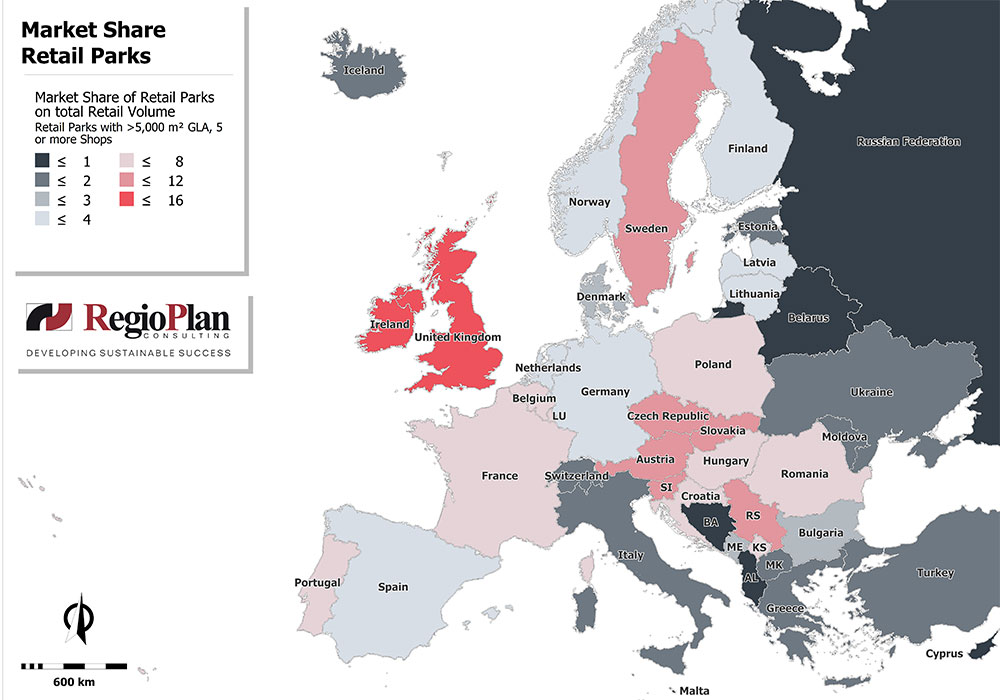

Retail parks present themselves as an important element of Europe’s retail structure. 5 % of total European retail volume is absorbed within retail parks.

The popularity of this asset class is quite differing among the European countries, depending on factors such as topography, population structure of cities, legal and planning framework, learnt customer behavior, demand of retailers with suitable concepts and so on.

The intensity by country varies accordingly. While retail parks generate market shares beyond 10 % in Ireland, UK and Sweden on the one hand, there is less than 1% absorption in Russia, Belarus or part of the Balkans. UK stands out within the largest European markets with a remarkably high retail park presence. In Italy, however, they have never had a great track record. Largest retail parks with GLA of over 100,000 sq m each are found in Spain, France and Poland; the smallest ones are found in Denmark, Swiss, Austria, and Finland.

Overall, 120 retail parks, with high probability of implementation, are planned all over Europe, which is the lowest value as seen within the last 20 years. On average, projected retail parks will be 21,000 sq m GLA, of which some significantly larger ones are planned in Russia.

Unlike in the past, the driving force of these developments are not anymore potential gaps of supply or demand of retailers, but mainly end-investors, searching for more suitable opportunities to invest. In a mid- to long-term perspective, the importance of retail parks will yet expand, even though the change of customer behavior (buzzword online shopping) will be a limiting factor.