BY MANUEL JAHN

We estimate Germany’s retail park market, consisting of 250 retail parks, to be worth around €12 billion based on object-specific sales area productivity and feasible rent-to-sales ratios. With a 20% share of current transaction volumes within retail real estate, retail parks have now assumed the status of a stand-alone asset class.

In the first half 2014 alone, €900 million was spent on this asset class, according to an evaluation of the transaction statistics of the large real estate brokers. These half-year figures show that around 7.5% of the entire market volume was traded – a figure that should rise to 10-15% by the end of the year. Assuming this market dynamic holds steady, retail parks would change ownership every 7-10 years on average.

Retail parks can already be regarded as a sustainable investment thanks to the increasing professionalization in this asset class, which is marked by higher-quality new buildings, a larger number of successful refurbishments, better-targeted tenant concepts, and a growing management quota. These numbers outshine previously favored shopping center investments and are awakening the interest of investors, particularly institutional ones.

TURNOVER POTENTIAL DIFFERS WIDELY

Retail parks are a meaningful retail real estate class; not just for investors, but also for retailers, who must also separate the wheat from the chaff when it comes to selecting viable locations. The size and turnover associated with these locations can differ enormously: For retail parks between 10,000 and 76,000 sq m of sales area, the turnover spread is from €15 million to just under €300 million per year.

The branch mix of retail parks is dominated by grocery offerings. GfK’s analysis of 250 retail parks in Germany revealed that the turnover share for groceries ranges from €2 million to €90 million, depending on the retail park concept. Fashion offerings generate turnover from €0.5 to €30 million p.a.

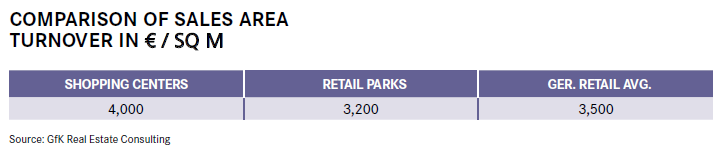

PROFILE OF THE AVERAGE CENTER

Our object analyses revealed that the average German retail park has around 19,600 sq m of sales area divided into 20 rental spaces that generate around €3,200 of gross turnover/sq m annually. On the basis of retail format and tenant specific rent-to-sales ratios, we calculated an average rental income potential of €12 per month per sq m. As such, the average sales area productivity is, as expected, still far removed from the average performance of a German shopping center, which, according to the GfK shopping center database, is around €4,000/sq m; but retail park performance is not far from the average performance of German retail, which is currently around €3,500 gross turnover/sq m of sales space.

The sales area productivity spread is disproportionately higher among retail parks compared to other managed retail real estate. We calculated sales area productivities that ranged from €1,110 at the weak end of the spectrum to €6,900 (gross) per sq m at the strong end. These differences are the result not just of the retail park’s quality, but also of the product-line mix. Retail parks dominated by established hypermarkets or large super-markets can achieve high to very high sales area productivities.

SO, WHERE ARE THE BEST RETAIL PARKS LOCATED?

Surprisingly, the best retail parks are not always located in central metropolitan areas. For example, one of the top retail parks we examined is located in a greenfield area. Established and successful retail parks that have been around a while were often erected in out-of-the-way commercial areas that are not well integrated into the city infrastructure and are often also invisible from main street axes. The fact that these have nonetheless established themselves in consumers’ minds during their decades of existence shows that there is no simple success formula — not even the real estate agents’ mantra: location, location, location. (And even “location” is not a simple concept, but rather a complex web of macro and micro market conditions as well as real estate object-specific features.) What we think comes closest to such a success formula for retail real estate is this:

x concept

Success = location x offering

x management

The point is: Retail real estate is not a homogeneous commodity. Even retail warehouses that are structurally nearly identical differ substantially.

But if one looks even deeper than these intricate details, a very simple and common success story emerges: The greater the ability to guarantee turnover for a given retail park, the more likely it is to hold on to tenants over the long term as well as draw attractive new tenants, thus extending the life cycle of the site. This means that the ultimate success of a retail park fundamentally depends on the drivers of demand, i.e. the end consumers.

ADDITIONAL INFORMATION

The complete white paper from Manual Jahn on retail parks can be accessed at www.gfk-geomarketing.com/download-retail_centers.

CONTACT

Manuel Jahn, Head of GfK Real Estate Consulting: manuel.jahn@gfk.com