Buoyed by a positive outlook among consumers and retailers alike, the majority of retail markets worldwide remained in good or very good shape during the second quarter of 2018. The ongoing economic boom is creating a number of lucrative growth markets that offer diverse investment opportunities. At the same time, the retail investment landscape is gradually being reshaped as the global upturn continues.

In particular, there is a widening gap between investor-friendly retail markets with good fundamentals and markets where the early warning signs first became apparent two years ago. As Union Investment’s Global Retail Attractiveness Index (GRAI) for Q2 2018 shows, the difference between the top performers and the weakest markets in Europe is now around 20 points. Compared with the previous analysis in Q4 2017, this gap is getting wider.

“The retail property sector is already experiencing a high degree of investor uncertainty,” said Henrike Waldburg, Head of Investment Management Retail at Union Investment: “So it’s vital to keep track of the very different patterns of regional development and to distinguish between markets that are trending positively for investors over the long term and ones that have severe structural deficiencies. The latest Global Retail Attractiveness Index can provide some useful pointers in this regard.”

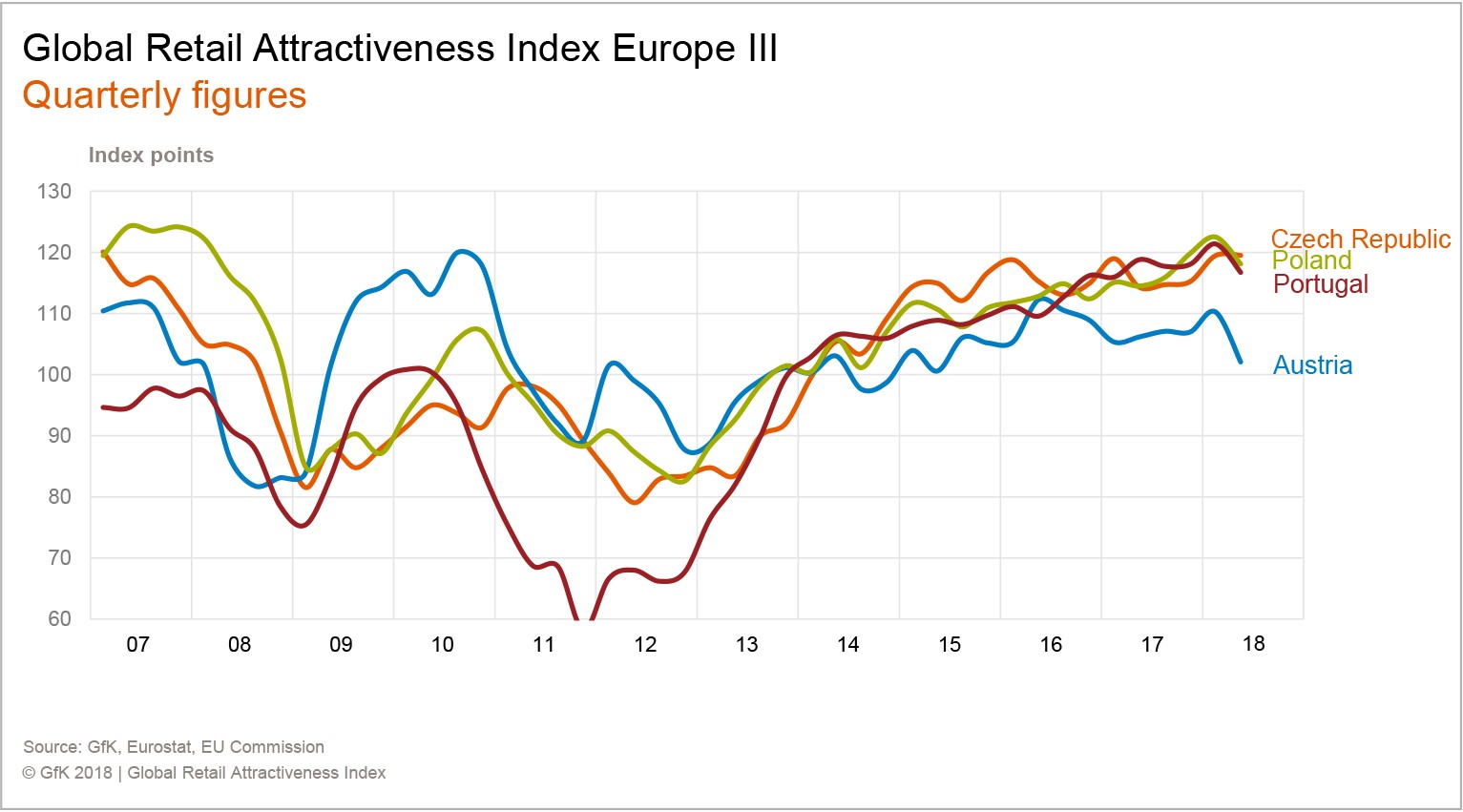

SHOOTING STARS: CZECH REPUBLIC AND POLAND

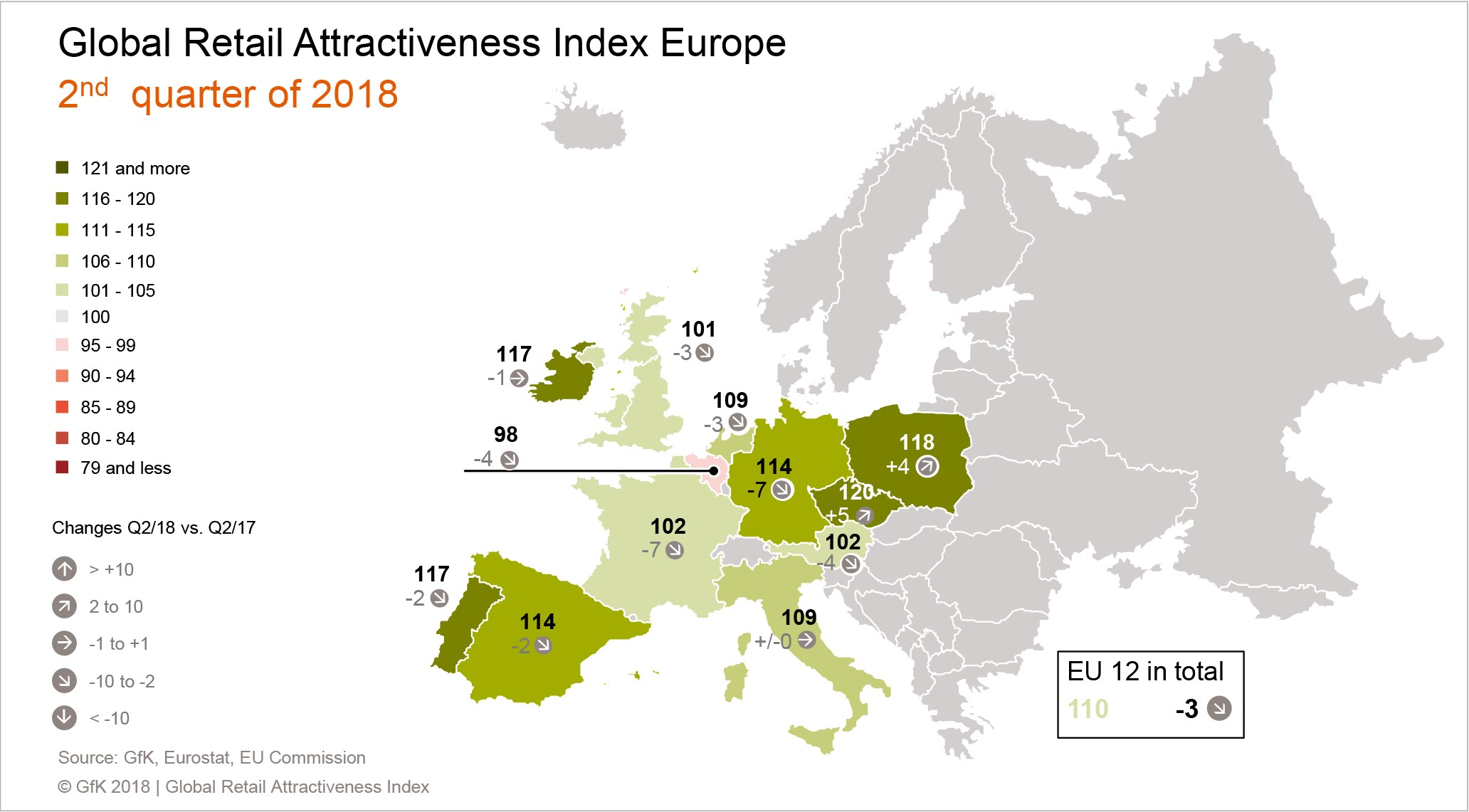

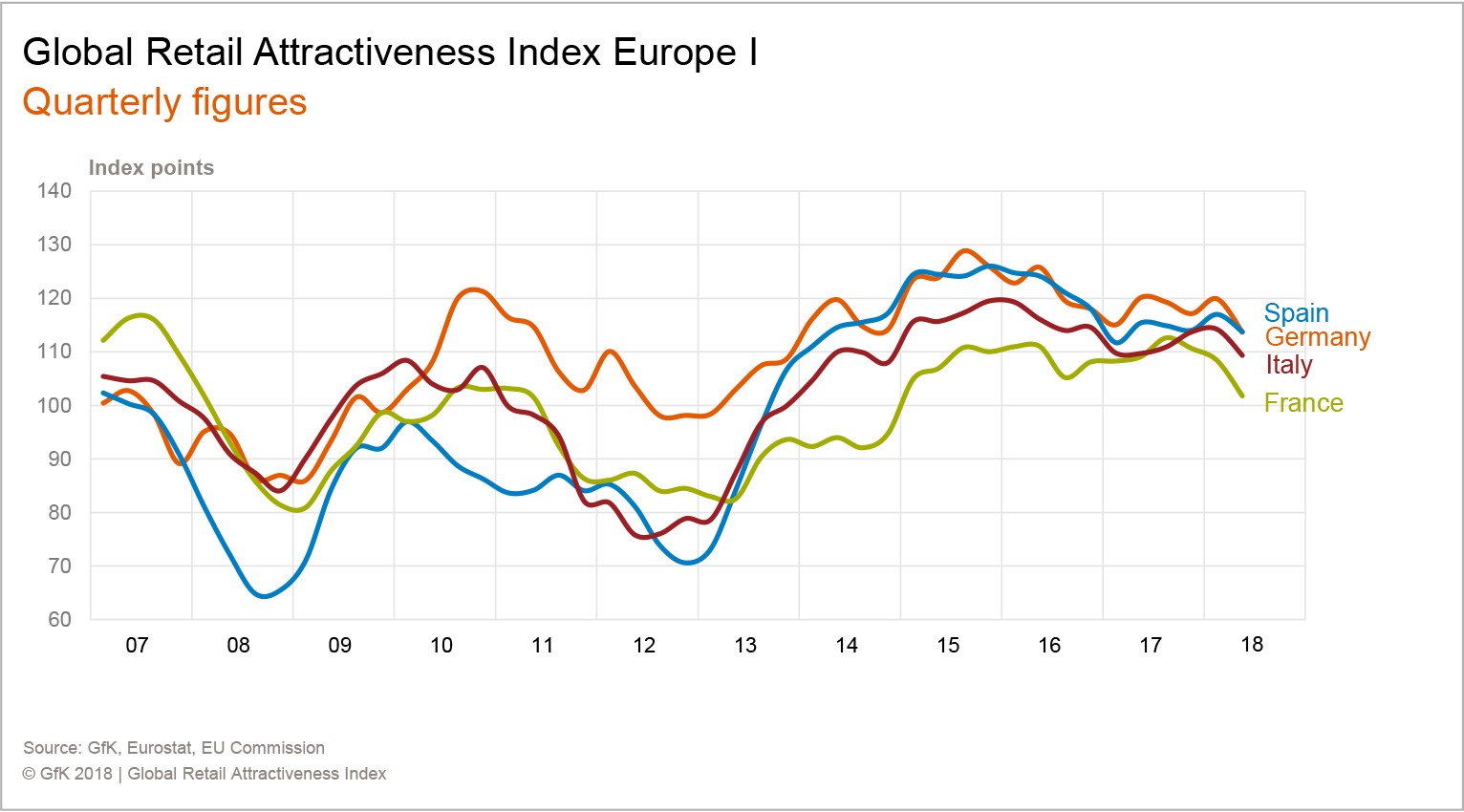

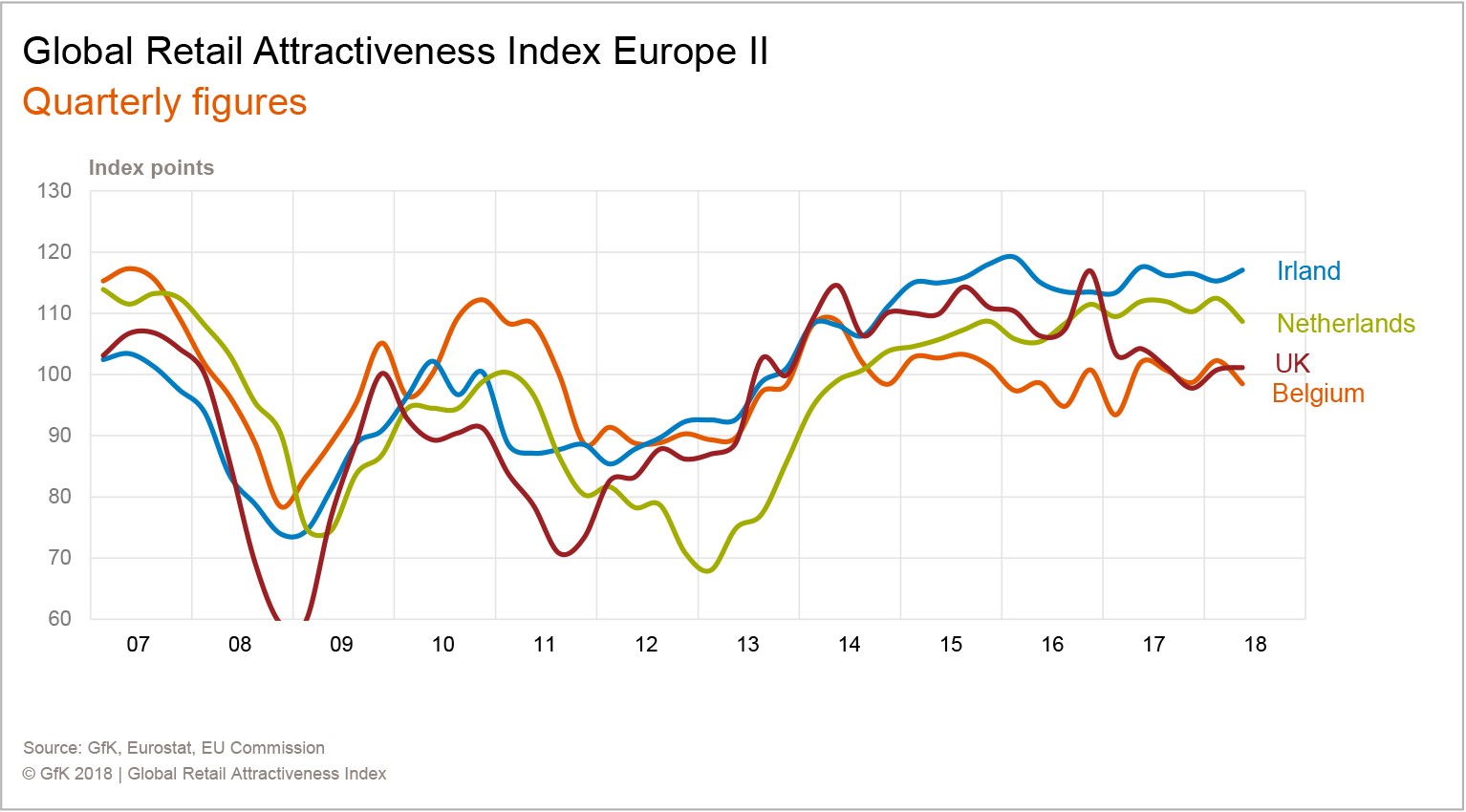

“One of the most important signals is the fact that the overall index for Europe in mid-2018 remains well above average at 110 points,” added Waldburg. “The main drivers for the EU-12 index are the further improvement in consumer confidence and the consistently positive mood among retailers.” According to the new GRAI, the most attractive retail markets in Europe in Q2 2018 are the two Eastern European countries, Poland and the Czech Republic, followed by two economies that were badly hit by the recent financial crisis: Ireland and Portugal. Once again, Germany remains one of the top five markets in Europe.

Of these five countries, only two have improved their index value year-on-year: the Czech Republic (+5 points) and Poland (+4 points) – the latter having been the top performer in Q4 2017. Significantly, the heaviest losses were suffered by mainland Europe’s economic heavyweights, Germany and France, each of which fell by seven points. While the slump in France was mainly due to inflation, Germany was hit by weak retail sales. Another change since the previous survey involves the new bottom three in the EU ranking: France, the UK and Belgium. At 99 points, Belgium is the only country in the current index to have slipped below the 100-point mark. The main reasons for this are the well below average outlook among Belgian retailers and weak growth in retail sales.

Having enjoyed comparatively stable growth since 2015, the 12-market European retail index lost ground during the past year, dropping a total of three points. This moderate decline was mainly due to the lack of growth in retail sales (sub-index: -12 points), and was evident in all 12 EU markets examined. The biggest losers in this particular subindex were Austria (-25 points), Portugal (-22) and Germany (-17).

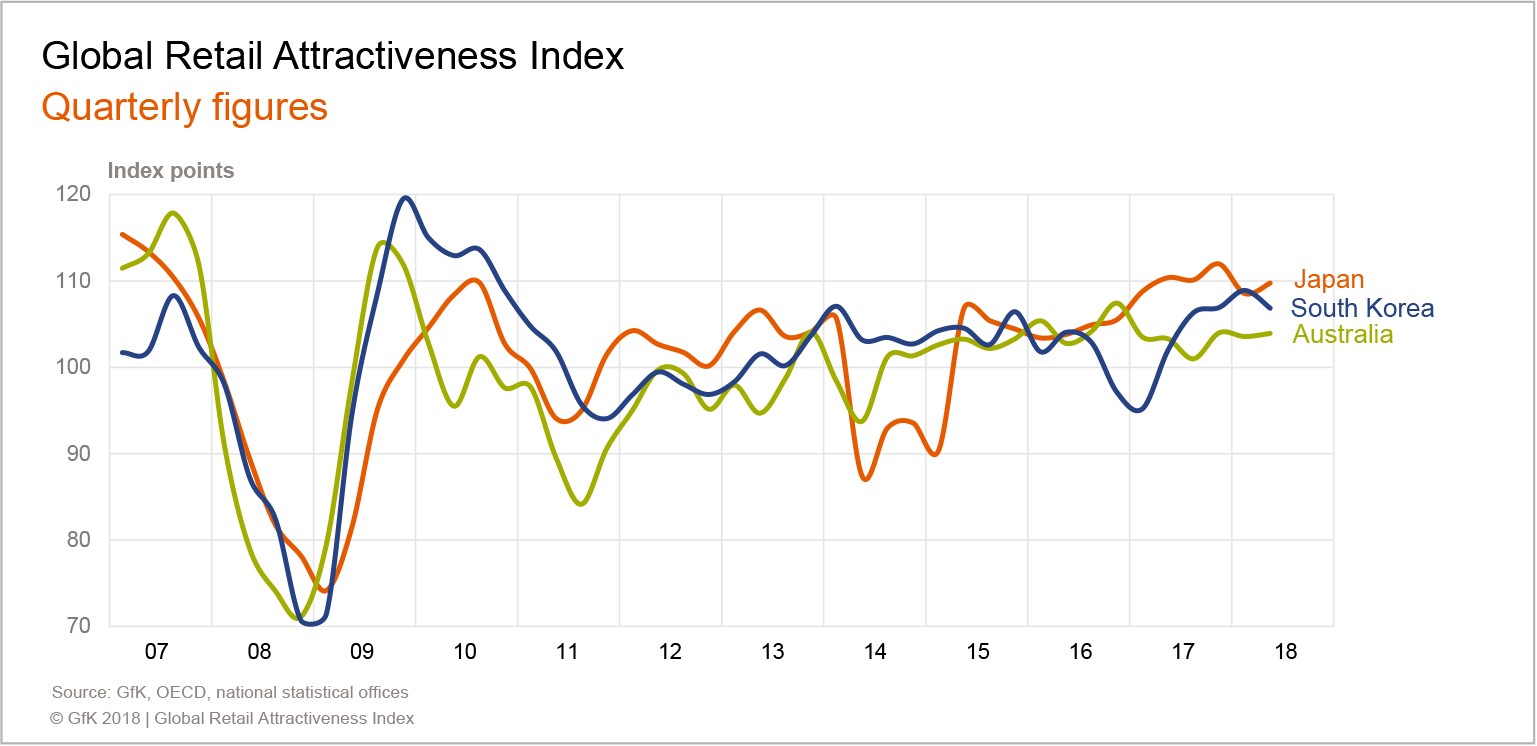

BIGGEST WINNER: SOUTH KOREA

The generally positive outlook in the relevant retail markets around the world is also apparent in the North American and Asia-Pacific indexes. With 111 and 108 points respectively, both are performing well above average. The North America index is up two points over the second quarter of 2017, while Asia-Pacific has risen by one. The international ranking is now headed by the US on 111 points (+2 points), followed by Japan on 110 points (-1 point) and Canada on 108 points (-4 points). The biggest winner is South Korea, which has climbed five points since Q2 2017. “As in Canada, inflation has had a strong dampening effect in the US,” said Henrike Waldburg. “However, the US is also experiencing a rise in retail sales, which combined with marked optimism on both the demand and supply side is creating an attractive investment environment. In Canada, by contrast, the hard factors inflation and retail sales are a reason for caution at the moment.”

With regard to transaction volumes, Union Investment expects retail investment over the next six months to be concentrated heavily in the top five European markets in the GRAI ranking plus the United States. “The European share of the in-vested capital will be around 75 per cent, perhaps even more,” said Henrike Waldburg. “In the other markets, we expect to see a further increase in caution among investors.”

Results for the 2nd quarter of 2018

ABOUT THE METHODOLOGY

Union Investment’s Global Retail Attractiveness Index (GRAI) measures the attractiveness of retail markets across a total of 17 countries in Europe, North America and the Asia-Pacific region. An index value of 100 points represents average performance. The EU-12 index combines the indexes for the following EU countries, weighted according to their respective population size: Germany, France, Italy, Spain, the United Kingdom, Austria, the Netherlands, Belgium, Ireland, Portugal, Poland and the Czech Republic. The North America index comprises the US and Canada, while the Asia-Pacific index covers Japan, South Korea and Australia.

Compiled every six months by market research company GfK, the Global Retail Attractiveness Index consists of two sentiment indicators and two data-based indicators. All four factors are weighted equally in the index, at 25 per cent each. The index reflects consumer confidence as well as business retail confidence. As quantitative input factors, the GRAI incorporates changes in the consumer price index (inflation) and retail sales performance. After standardisation and transformation, each input factor has an average value of 100 points and a possible value range of 0 to 200 points. The index is based on the latest data from GfK, the European Commission, the OECD, Trading Economics, Eurostat and the respective national statistical offices. The changes indicated refer to the corresponding prior-year period (Q2 2017).

KEY FACTS

RETAIL ATTRACTIVENESS INDEX EUROPE

Overall, the Retail Index in Europe remained at an above-average level of 110 points in the second quarter of 2018.

Sentiment indicators continued to be key drivers in mid-2018. Both consumer sentiment (122 points) and retail sentiment (114 points) significantly contributed to this good level.

Conversely, hard factors such as inflation (102 points) and retail sales (100 points) only made a below-average contribution to the overall index.

The index lost some ground during the course of last year. Compared to the second quarter of 2017, the drop amounted to three points. This is primarily due to the more moderate development of retail sales, whose sub-index has dropped 12 points over the last four quarters. Retail sentiment also contributed, albeit below average, with a drop of two points.

By contrast, consumer sentiment (+3 points) and inflation (+1 point) made moderately positive contributions to the development of the overall index.

At the country level, the two Eastern European countries, the Czech Republic (120 points) and Poland (118 points), are currently in the lead, followed by the former crisis countries of Ireland and Portugal (117 points each).

In the second quarter of 2018, Belgium, the only European country below the 100-point mark with 99 points, came in at the tail end of the group. A significantly belowaverage sentiment among retailers (91 points) and retail sales (89 points) are responsible for this weak development.

Only two countries, the Czech Republic (+5 points) and Poland (+4 points), showed a slightly positive development during the quarter. Two economic heavyweights in Europe, Germany and France, recorded the largest losses of seven points each.

Sign up for our ACROSS Newsletter. Subscribe to ACROSS Magazine.