There is currently no shortage of apocalyptic scenarios when it comes to the “bricks and mortar” retail sector. A weaker economy and increasing signs of a cyclical downturn are providing ammunition for the prophets of doom rather than arguments for investors looking to buy. At a time when entire markets and sub-sectors are being written off and some professional investors are simply giving up, it is nevertheless helpful to focus on the positive signals coming from some European retail markets.

“Investors tend to punish markets too severely due to political turmoil, yet the reality in some markets, such as Italy or Spain, is rather different. There is still scope in Europe for opportunistic investments in the current market environment,” said Henrike Waldburg, head of Investment Management Retail at Union Investment.

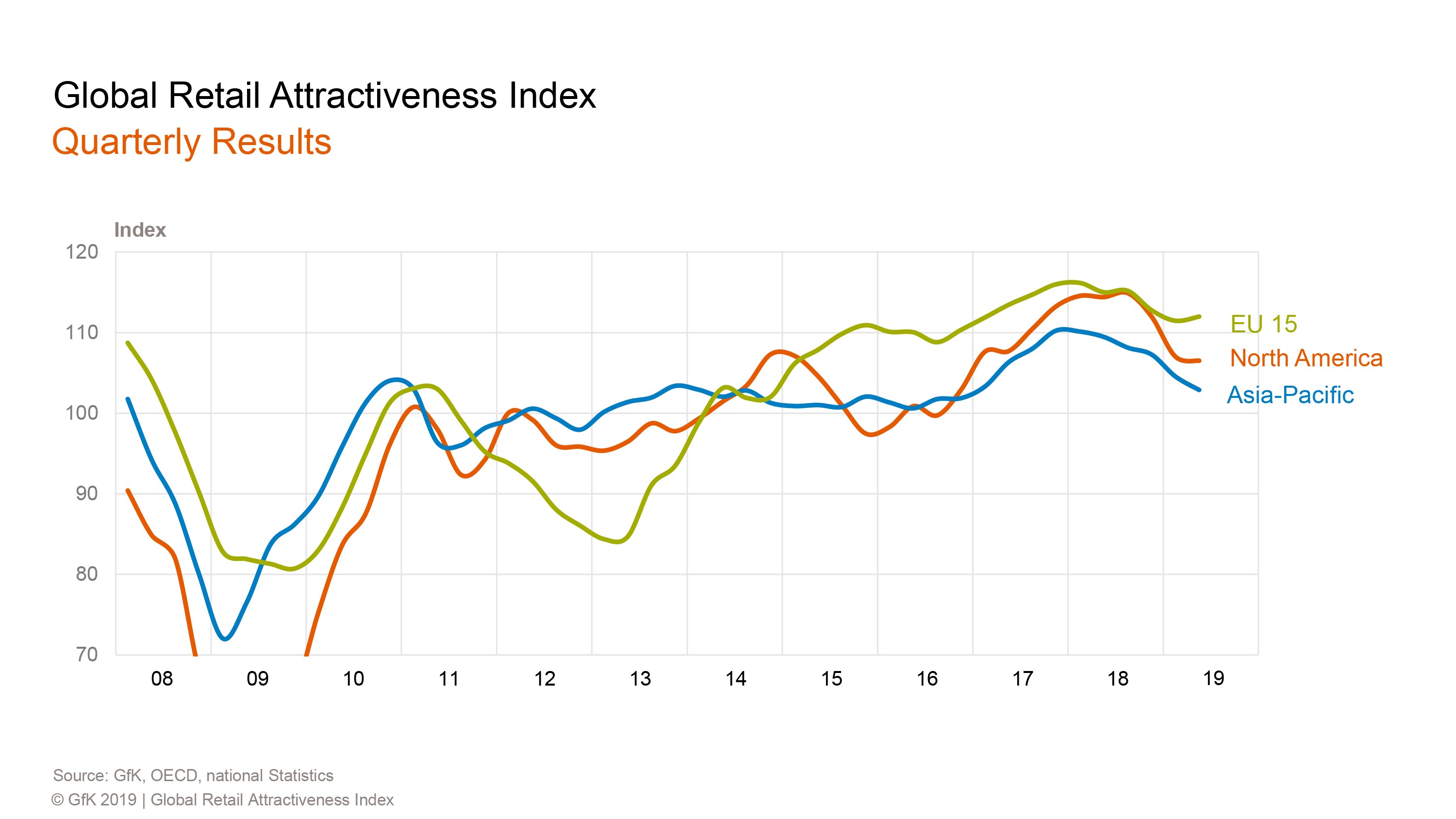

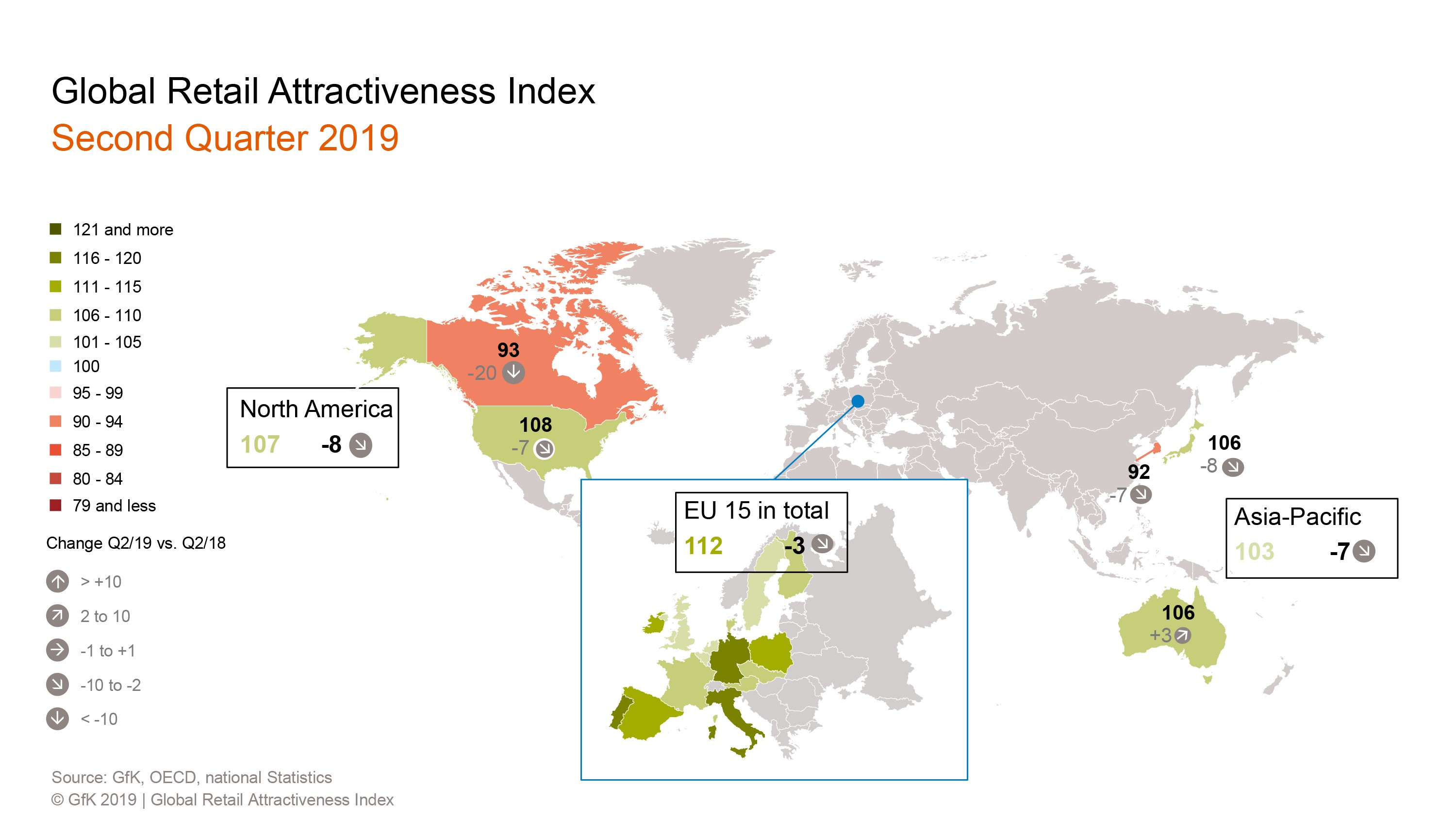

As the latest Global Retail Attractiveness Index (GRAI) compiled by Gfk and Union Investment shows, most retail markets in Europe are fundamentally intact. While trade disputes, the Brexit debate and a general economic slowdown have impacted consumer and retailer sentiment, the retail index for the 15 largest European markets held up relatively well in the second quarter of 2019. The EU-15 index remains above average, at 112 points, with a slight drop of three points compared to the second quarter of 2018 (115 points). The same applies to the North America index (107 points; -8 points) and Asia-Pacific index (103 points; -7 points). European job markets are highly supportive. The relevant indicator stands at 115 points, confirming the robustness that has been a feature for five years now. The labour markets in the Netherlands, Portugal, Finland and Belgium stand out in particular. The associated strong consumer sentiment across large parts of Europe helps to underpin the retail index. At 116 points compared with the previous year’s figure of 122, the relevant indicator has softened somewhat, however.

Reflecting the gloomy economic picture, the more pessimistic sentiment among retailers indicated by a weak value of 109 points has caused a slight widening of the gap from the index’s previous peak of 116 points, recorded in the first quarter of 2018. “Looking at the four individual indicators, the highest volatility and greatest variation are in retailer sentiment data. In the Netherlands, Austria, Belgium and – as one would expect -the UK, where retailers’ concerns have long been reflected in the index, current trends should be seen as a warning signal,” said Henrike Waldburg.

Portugal and Germany confirm top spots

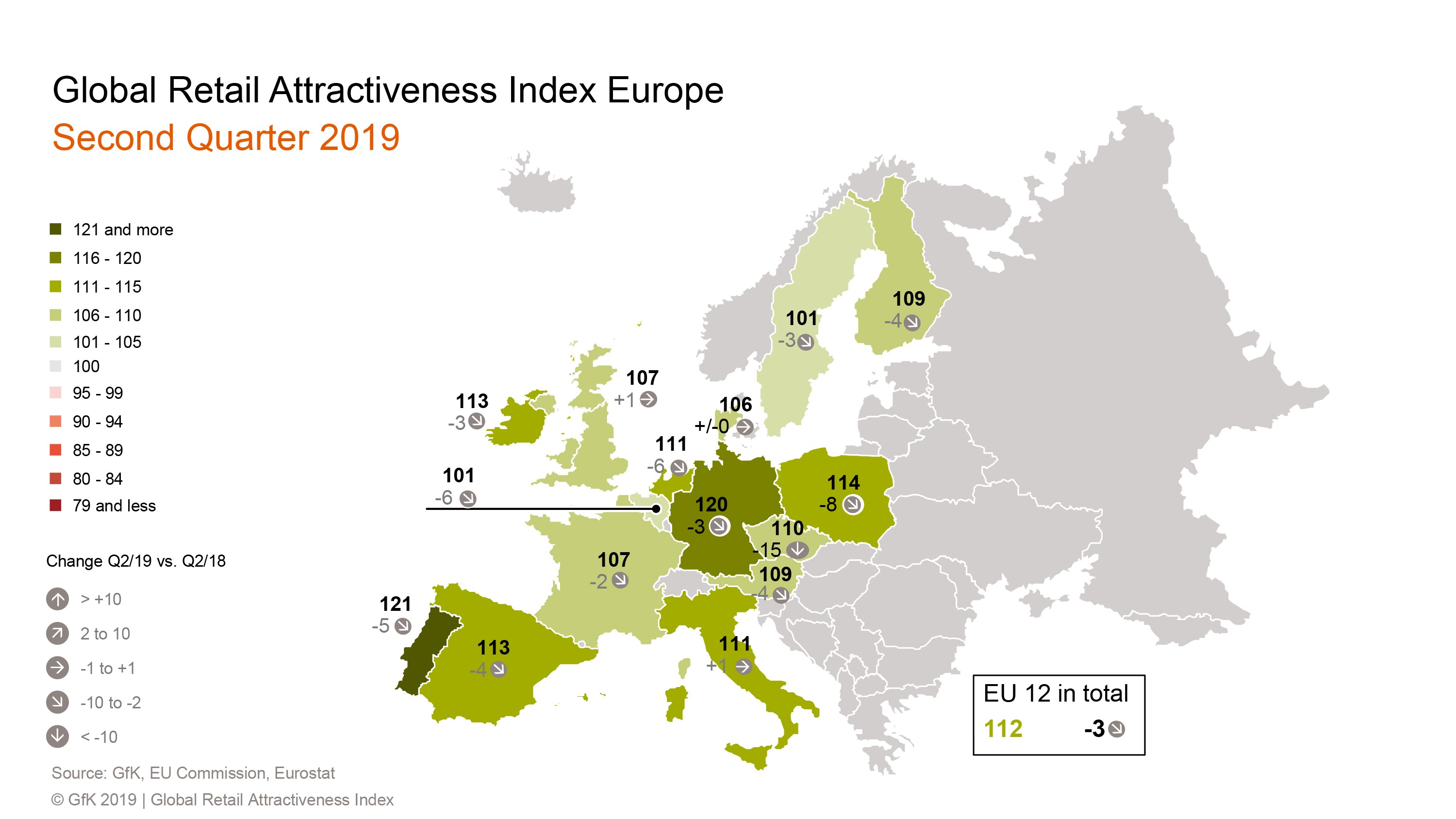

The GRAI provides encouraging signs for a number of markets which score highly across all four indicators from an overall strong base. Portugal in particular continued to perform well. At 121 points (-5 points compared to the second quarter of 2018), Portugal held on to the top slot in the EU-15 index. Although the country has seen a decline in consumer sentiment, the Portuguese are again posting excellent results for labour market data and retail sales.

Germany also continues to rank among the top performers, with 120 points (-3 points).”Buoyant consumer sentiment in Germany, backed by solid retail sales figures and labour market data, is encouraging foreign institutional investors to consider the German retail sector for opportunistic investments, despite stagnating rents,” said Henrike Waldburg.

Poland has established itself among the top five in Europe, albeit trailing the top two somewhat. At 114 points (-8 points), the country is once again making an above-average contribution to a healthy EU-15 index. Having said that, it is important to be aware of labour market trends and the sharp drop in retailer sentiment, as well as tax issues, according to Henrike Waldburg. Poland also has a lot of catching up to do in the online sector, a factor that will have a delayed impact on the country’s retail landscape, she added.

The former “problem children” in the Eurozone periphery have likewise become firmly established in the index. At 113 points each, Spain and Ireland confirmed that they are on the right track, having further narrowed the gap to the leading trio. “Spanish retailers, especially in Madrid and Barcelona, have been posting positive data for around four years now. Spain’s share of exposures is likely to rise significantly from its current very low level over the medium term,” commented Henrike Waldburg.

Caution needed in the Czech Republic, Belgium and Sweden

Elsewhere, notable changes in national indices mean that investment decisions should be subjected to careful scrutiny. The biggest losses in the course of the year were posted by the Czech Republic. Six months ago it was ranked in the top group, above the German retail market. The significant decline across all four indicators dragged the Czech Republic down by 15 points to 110, relegating it to eighth place in the latest EU-15 ranking.

In Belgium and Sweden too, the retail investment markets are likely to remain becalmed. A score of 101 points each puts these two countries joint bottom in the EU-15 index in the second quarter.

“Weak sentiment among Belgian retailers can now be described as chronic. Even the UK is currently posting better figures,” said Henrike Waldburg.

What is striking is that continuing growth in retail sales initially halted a further collapse of the UK index in the second quarter of 2019. By adding one point each, the UK and Italy are the only countries that have improved their performance over the same period of the previous year. At 107 points in the second quarter of 2019, the UK was on a par with France, whose retail markets softened slightly (-2 points) to reach a more or less average level. The score for the UK amid the turmoil of Brexit only seems surprising at first sight. “The Brexit decision has not created a new reality yet, either for consumers, the labour market or for retail sales. If the UK experiences the expected dramatic slump in GDP, the retail sector will be the most directly affected, along with logistics and probably also the hotel industry,” noted Henrike Waldburg.

The expansion of the GRAI to include the Nordic countries Denmark, Finland and Sweden (EU-15) provides an even more comprehensive picture of trends in the wider European market. The new GRAI with its unemployment indicator and 12-month rolling retail sales figures tracks the diverging trends in the European and international retail markets with even greater precision, thereby providing investors with even better insights.

METHODOLOGY

Union Investment’s Global Retail Attractiveness Index (GRAI) measures the attractiveness of retail markets across a total of 20 countries in Europe, North America and the Asia- Pacific region. An index value of 100 points represents average performance. The EU-15 index combines the indexes for the following EU countries, weighted according to their respective population size: Denmark, Finland, Germany, France, Italy, Spain, Sweden, the United Kingdom, Austria, the Netherlands, Belgium, Ireland, Portugal, Poland and the Czech Republic. The North America index comprises the US and Canada, while the Asia-Pacific index covers Japan, South Korea and Australia.

Compiled every six months by market research company GfK, the Global Retail Attractiveness Index consists of two sentiment indicators and two data-based indicators. All four factors are weighted equally in the index, at 25 per cent each. The index reflects consumer confidence as well as business retail confidence. As quantitative input factors, the GRAI incorporates changes in the unemployment rate and retail sales performance (rolling 12 months). After standardisation and transformation, each input factor has an average value of 100 points and a possible value range of 0 to 200 points. The index is based on the latest data from GfK, the European Commission, the OECD, Trading Economics, Eurostat and the respective national statistical offices. The changes indicated refer to the corresponding prior-year period (Q2 2018).

ACROSS MAGAZINE IS NOW ALSO AVAILABLE AS AN E-PAPER!

Try it and get free access until the end of November 2019. Please use the voucher code Across for free access until the end of November 2019.