European retail markets resilient in face of global economic downturn

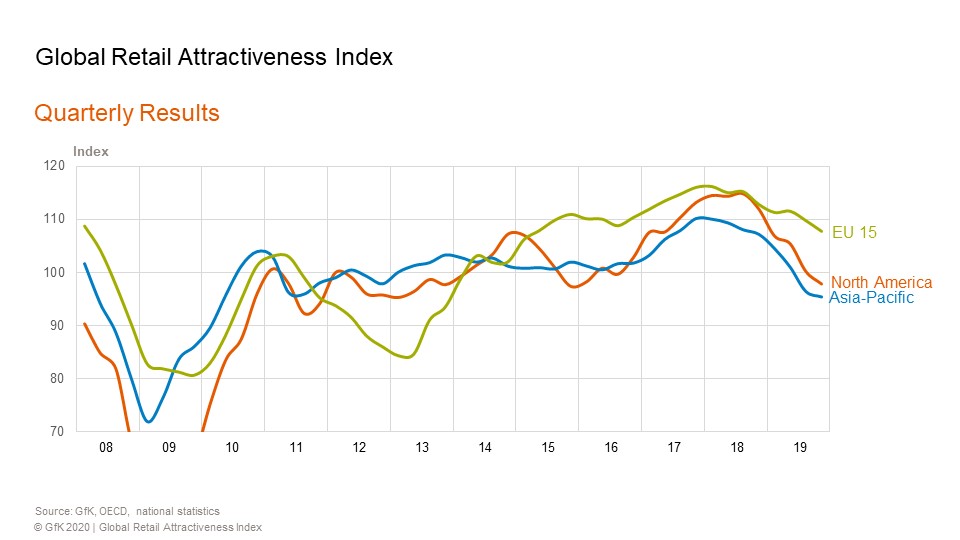

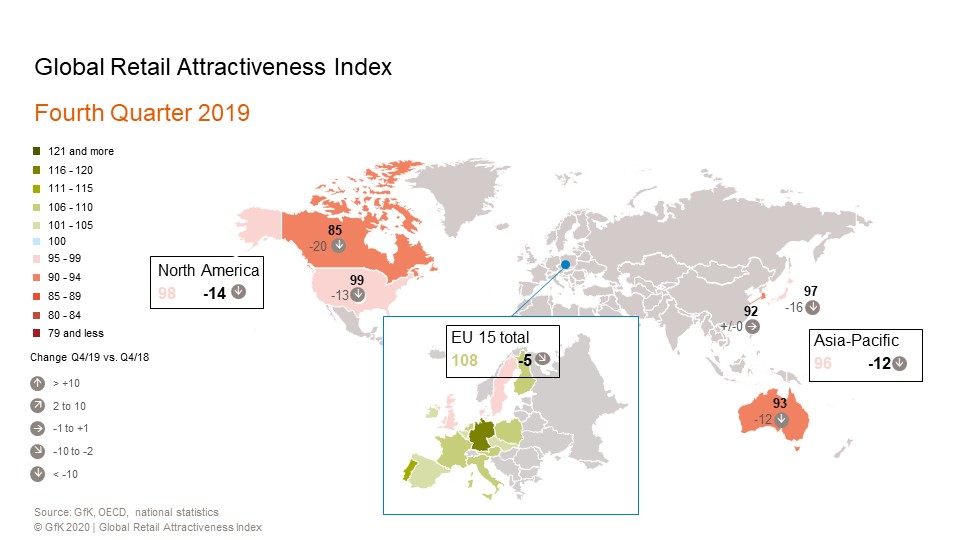

European retail markets are still doing well despite declining economic momentum. The Global Retail Attractiveness Index (GRAI) for the 15 biggest retail markets, which is compiled jointly by Union Investment and GfK, again fell slightly by 5 points compared with the previous year. But at 108 points it still remains significantly above the long-term average. Among the stabilisers are the major economies, which continue to make Europe a safe haven for real estate investors overall. Germany experienced only a slight decline (-5 points) compared to Q4 2018 and remains the strongest retail market with 116 points, while Italy demonstrated its renewed robustness with an unchanged 110 points. France actually improved and is the only country among the European top 15 to record an increase (+6 points). The index lost some ground in the UK, Denmark and Sweden as a result of weaker growth.

Overall, however, the GRAI in Europe is significantly higher than the index in North America (98 points) and in Asia-Pacific (96 points), where the global economic slowdown and ongoing trade dispute between the US and China have had a profound impact. Despite the downward trends also being seen in Europe, the gap between North America and Europe widened during the year from 1 to 10 points, while the gap between Asia and Europe is now 12 points.

“The labour market and consumer sentiment were the main sources of support in Q4 2019 and are key to the overall strong showing of the index in Europe. By contrast, retail sales performance is having a dampening effect. In the current environment, it remains a major challenge to find good investments with secure cash flows that also offer the prospect of appreciation,” said Henrike Waldburg, head of Investment Management Retail at Union Investment.

Polarising landscape

The subdued economic backdrop was an adverse factor for nearly all retail segments including online retail and was leading to greater market polarisation, said Henrike Waldburg. This made it necessary to be even more cautious when selecting assets.

“Retailers in smaller, non-dominant schemes in secondary and tertiary cities will face difficulties. In contrast, dominant shopping locations with attractive offerings that reflect changing consumer behaviour and customer needs will find it easier to cope with the structural changes taking place in retail.”

She cited the example of the Puerto Venecia shopping resort in Zaragoza, one of the three busiest shopping malls in Spain. “The average dwell time here is three hours, which is one of the reasons we decided to invest here last year.” In the current economic environment, retail parks have also proved to be particularly resistant to online competition and therefore able to hold their value, especially those buoyed by major food anchors on long leases. “Germany still has some catching up to do, especially when it comes to community shopping centres,” said Henrike Waldburg.

In the GRAI, the top three countries are currently Germany with 116 points, Portugal with 115 points and Italy with 110 points. Poland and France also score above average in the European index, with 109 points each. The lowest placed country in Q4 2019, with just 96 points, is Sweden. Denmark and the UK are also below average, with 97 and 98 points respectively. During the year, the Czech Republic (-14 points), Poland (-12 points), the Netherlands and Portugal (-10 points each) saw the sharpest declines in the Retail Index.

METHODOLOGY

Union Investment’s Global Retail Attractiveness Index (GRAI) measures the attractiveness of retail markets across a total of 20 countries in Europe, North America and the Asia-Pacific region. An index value of 100 points represents average performance. The EU-15 index combines the indexes for the following EU countries, weighted according to their respective population size: Denmark, Finland, Germany, France, Italy, Spain, Sweden, the United Kingdom, Austria, the Netherlands, Belgium, Ireland, Portugal, Poland and the Czech Republic. The North America index comprises the US and Canada, while the Asia-Pacific index covers Japan, South Korea and Australia. Compiled every six months by market research company GfK, the Global Retail Attractiveness Index consists of two sentiment indicators and two data-based indicators. All four factors are weighted equally in the index, at 25 per cent each. The index reflects consumer confidence as well as business retail confidence. As quantitative input factors, the GRAI incorporates changes in the unemployment rate and retail sales performance (rolling 12 months). After standardisation and transformation, each input factor has an average value of 100 points and a possible value range of 0 to 200 points. The index is based on the latest data from GfK, the European Commission, the OECD, Trading Economics, Eurostat and the respective national statistical offices. The changes indicated refer to the corresponding prior-year period (Q4 2018).