The GfK study is based in part on anonymous and aggregated channel-specific purchasing data from GfK’s consumer panels for the product groups in question. Using geostatistical comparisons, GfK’s experts determined the regional online potential for 17 product groups for all regions in Germany. The data reveal the regional distribution of online potential for product lines down to the level of Germany’s municipalities and postcodes.

“Our data on regional online potential gives stationary and online retailers valuable insights into the diverse opportunities and challenges in their active markets,” explains Simone Baecker-Neuchl, Head of the GeoInsights division of GfK’s Geomarketing solution area. “As such, the new study provides a key decision-making basis for numerous company areas, from marketing and category management to expansion endeavors.”

Below are findings from the new GfK study on differences in the regional distribution of online potential for four product groups:

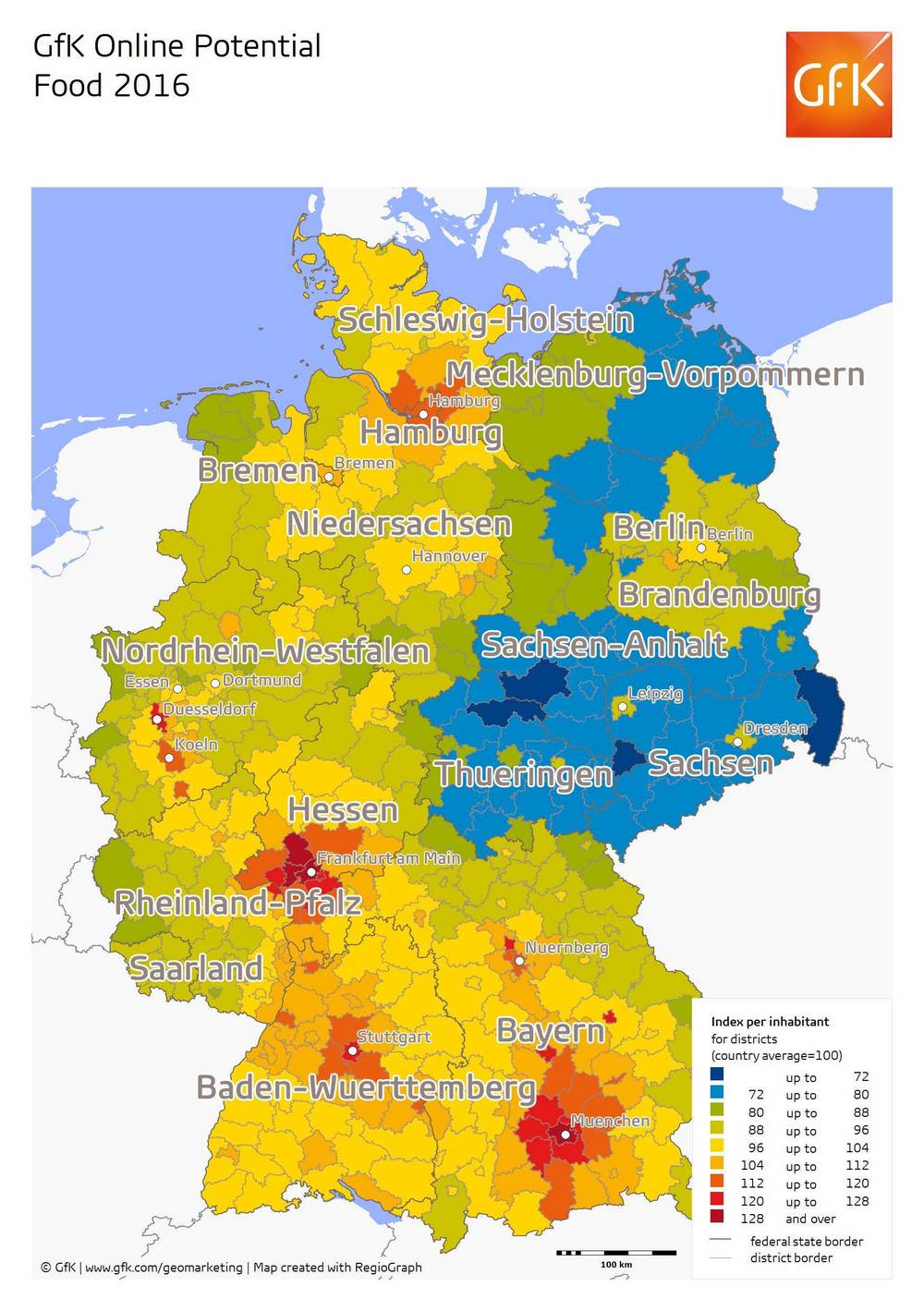

Food

While the distribution of total food purchasing power (i.e. stationary and online potential combined) is very balanced, there are more pronounced regional differences in the distribution of online potential. Ordering food items online is not yet a wide-spread practice in Germany.

While the distribution of total food purchasing power (i.e. stationary and online potential combined) is very balanced, there are more pronounced regional differences in the distribution of online potential. Ordering food items online is not yet a wide-spread practice in Germany.

Even so, there are regions of significant interest: The online potential for food items is substantially above average in large cities such as Munich, Frankfurt, Stuttgart, Hamburg, and Berlin, as well as in the surrounding areas.

In contrast to the total purchasing power for food, online potential for food is especially concentrated in the city centers of these metropolitan areas. This has both supply and demand reasons. One explanation is that the online food offering is larger in cities.

Online food retail generally requires significant logistical effort, but the shorter distances within cities reduce this factor. Another reason is that start-ups often test new concepts in large cities and limited distribution areas.

An additional explanation is that large cities have high concentrations of target groups for whom the delivery cost of online food orders is not a deterrent, either because they have limited time to shop or are simply more open to trying innovative retail offerings.

There is a notable difference between the potential in the western and eastern parts of Germany: The areas outside of cities in Germany’s eastern federal states have a significantly below-average online potential for food, which is in accordance with the lower total retail purchasing power in these regions.

There are also fewer online food suppliers in these areas, however. It is thus unclear whether supply or demand issues are ultimately the cause of the below-average online food potential in these regions.

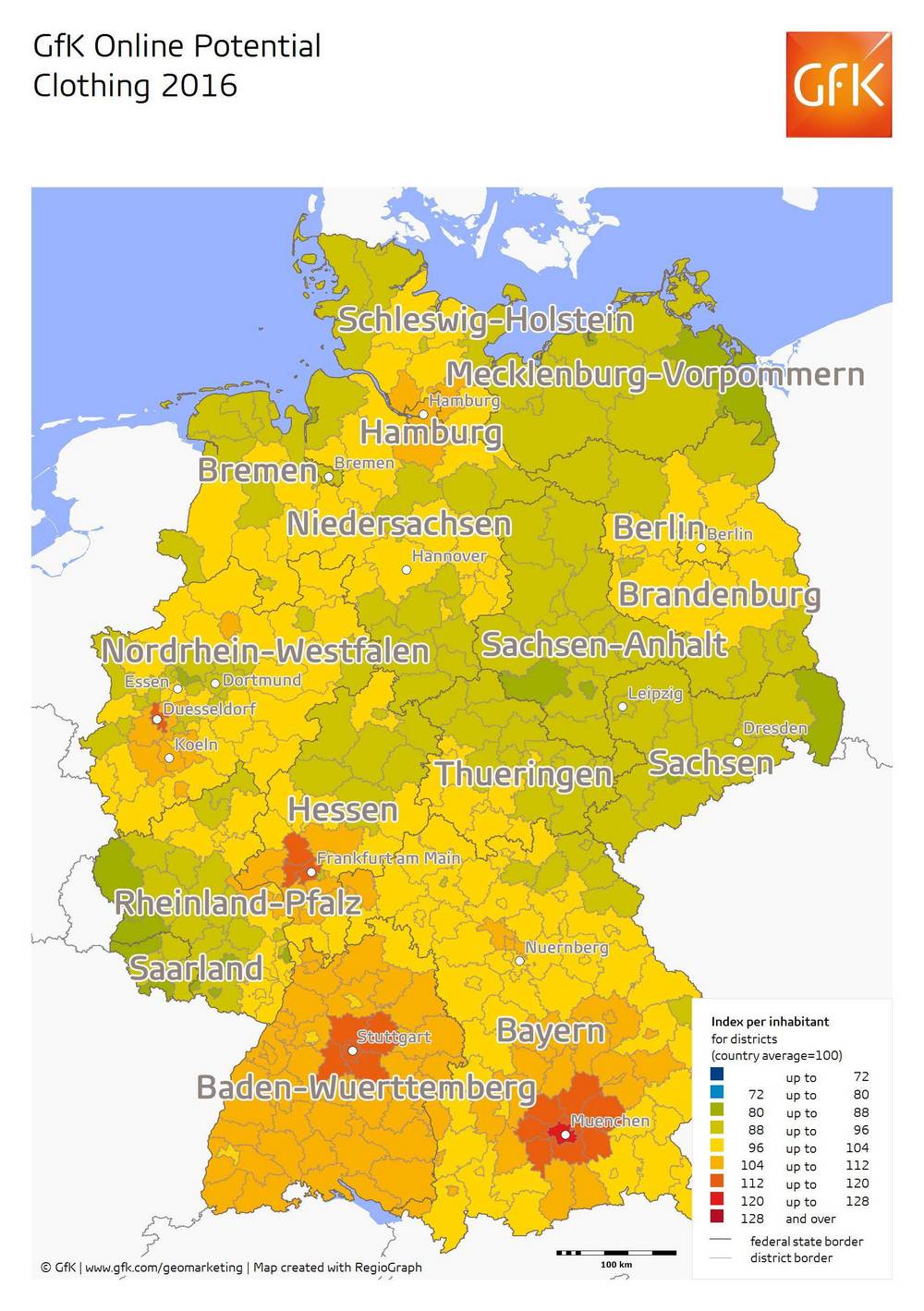

Clothing

At first glance, the geographic distribution of online potential for clothing appears to track with that of general purchasing power: Inhabitants in the greater metropolitan areas of Munich, Rhine-Main, Stuttgart, and Düsseldorf have an above-average online clothing potential.

At first glance, the geographic distribution of online potential for clothing appears to track with that of general purchasing power: Inhabitants in the greater metropolitan areas of Munich, Rhine-Main, Stuttgart, and Düsseldorf have an above-average online clothing potential.

Compared to the overall purchasing power for clothing, however. online potential is less pronounced in these large cities. This is due to the wide-ranging stationary retail offering in large cities and the generally higher expenditures on clothing in these areas.

On the whole, regional differences in online potential for clothing are relatively minor. Online shopping for clothing is already very wide-spread in Germany, with offerings catering to every consumer preference.

Online clothing offerings sometimes also compensate for gaps in stationary retail. This is particularly true in rural areas, which intensifies the competition between online and offline retail there. By contrast, the comprehensive stationary offering in larger cities dampens this competition.

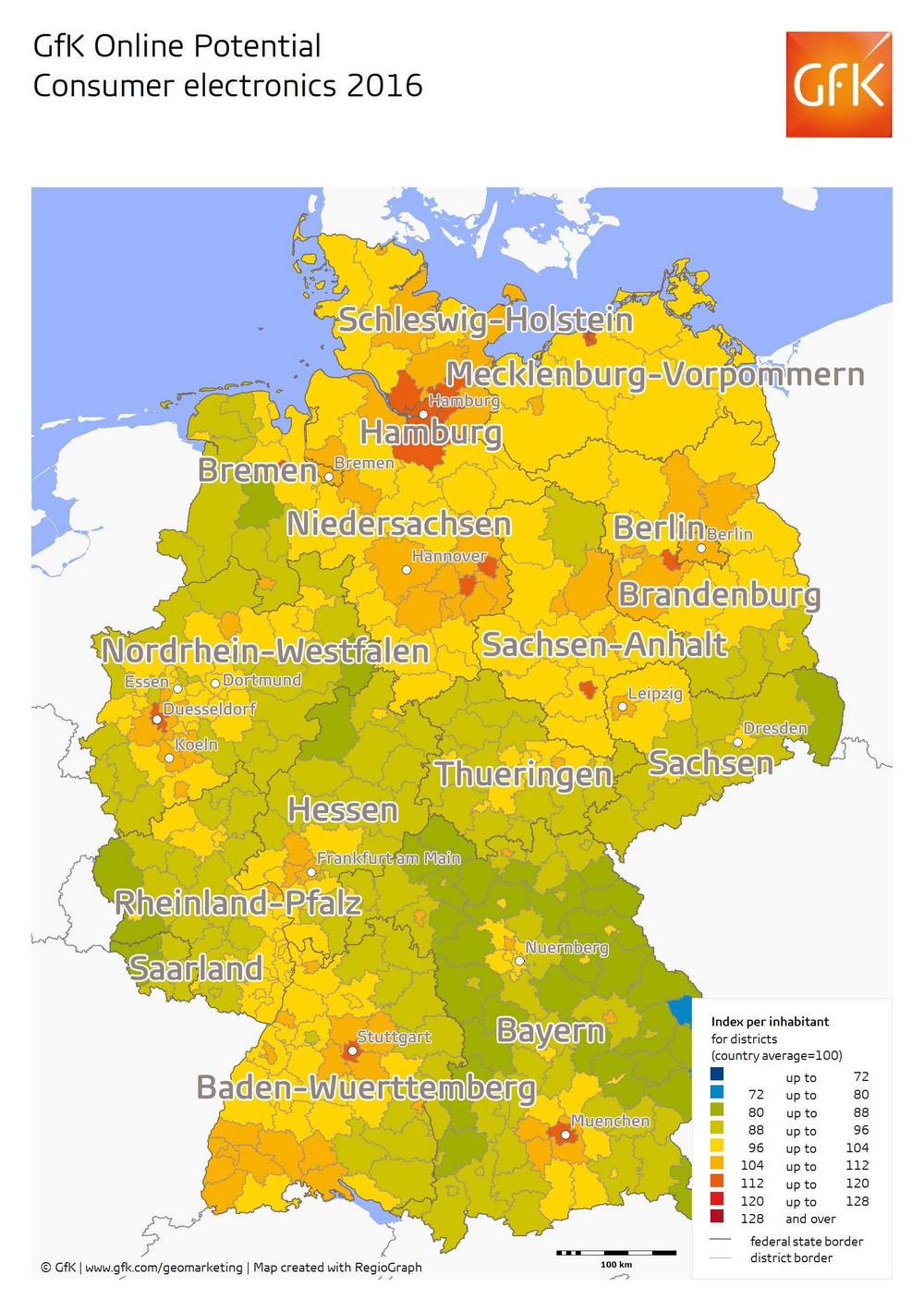

Consumer electronics

As in the case of clothing, there are only moderate differences in the regional distribution of online potential for consumer electronics.

As in the case of clothing, there are only moderate differences in the regional distribution of online potential for consumer electronics.

Consumer electronics products have long been offered and purchased online, so consumers routinely consider this channel when making purchases. Given the lower general purchasing power in many eastern regions of Germany, the strong online and total potential for consumer electronics in these areas is notable.

The study also shows high online potential in Germany’s main metropolises as well as in cities such as Braunschweig, Bremen, and Halle/Leipzig, despite the broad consumer electronics stationary offering in these areas.

This contrasts with the pattern of online potential for clothing, which is prominent only in the most populous cities. Reasons for this include the generally above-average affinity for technology products in densely populated areas as well as the greater comparability and price sensitivity of consumer electronics products.

The online potential for consumer electronics to a certain extent influences the pattern for overall purchasing power for this segment because online market shares are already relatively high.

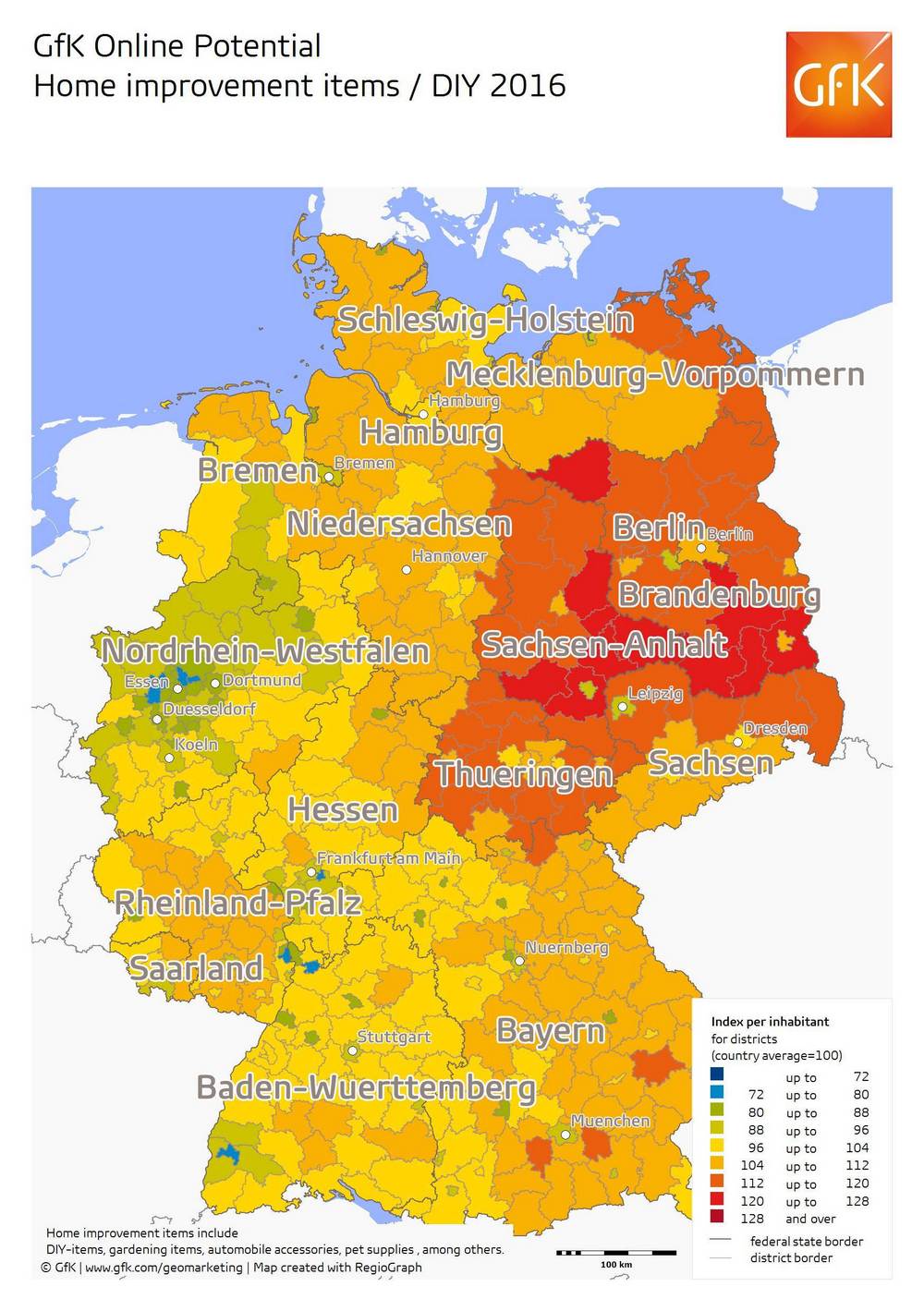

DIY products

This segment has an entirely different regional distribution of potential compared to the previously considered product groups.

This segment has an entirely different regional distribution of potential compared to the previously considered product groups.

The total purchasing power for DIY is generally higher in eastern and northern regions of Germany. Interestingly, the online potential for DIY products even further outpaces the national average in these areas.

This segment exhibits a stark urban-rural divide, which is apparent in the distribution of both the total purchasing power and the online potential. This potential is lower in cities and higher in rural regions, which is due to the larger per-capita living and garden spaces in areas outside of cities.

The unusually high online potential in eastern Germany is also a reflection of regional behavior patterns and values such as autonomy and neighborliness.

Also, the lower overall purchasing power in these areas means that those unable to afford hiring craftspeople tend to do this work themselves. This fact additionally strengthens the online potential for DIY products, because the online offering can be used to compare prices among retailers directly.

About the study

Available as of October 2016, this first-ever GfK study on regional online potential offers insights on the distribution of potential for 17 product lines via the online channel in Germany.

The study also draws on aggregated and anonymized information on the online and offline purchases of a representative sample from GfK’s consumer panels of approximately 30,000 households in Germany.

On the basis of this consumer information, GfK’s Geomarketing solution area determines the regional, product line-specific online purchasing power through socio-demographic comparisons and geostatistical modeling.

About GfK