by Romina Jenei, RegioPlan

Our focus is on the development of purchasing power in European countries, which has been vigorously shaken up by COVID-19. These notable changes have fluctuated between laissez-faire and drastic measures, depending on the severity of the pandemic and the respective governments’ strategies. Let us, therefore, take a closer look at the most affected countries in Europe and what it all means for our future.

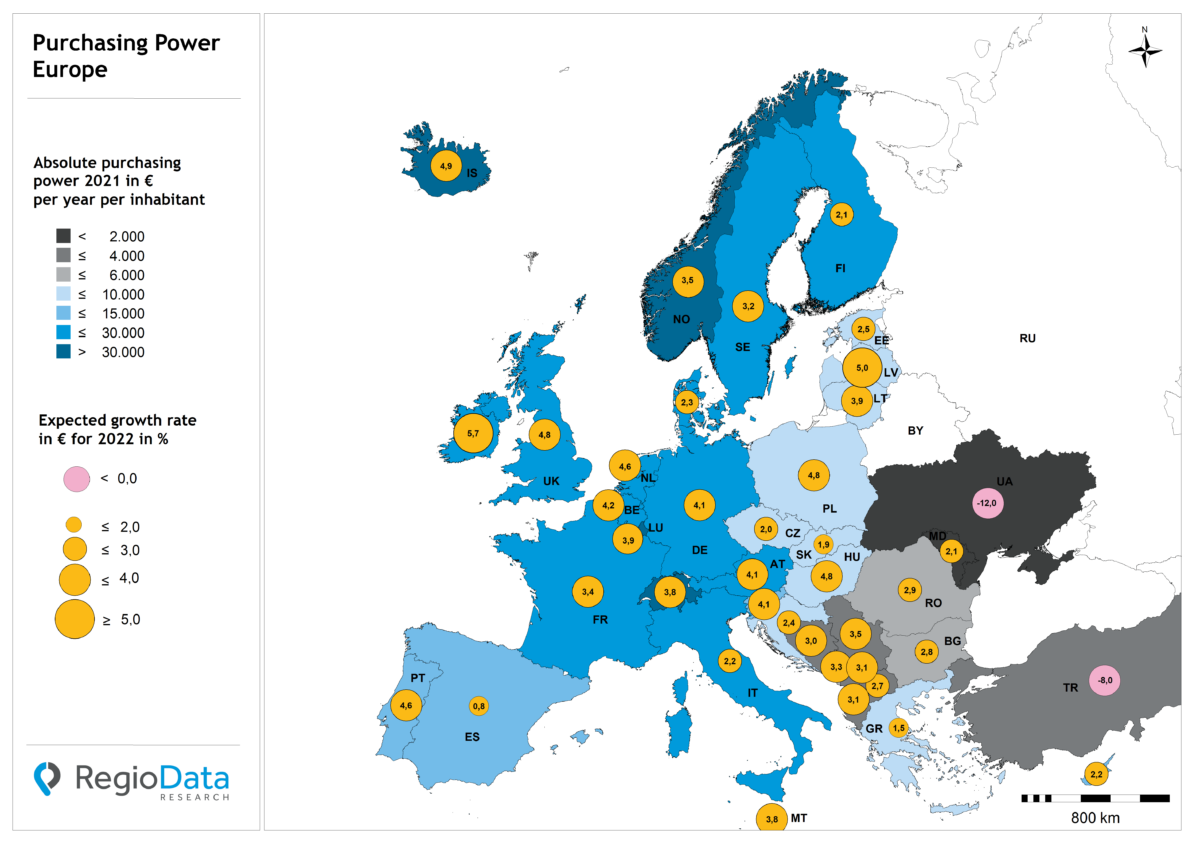

Significant Declines and Slight Increases

What has remained the same are the four countries with by far the richest citizens: Switzerland, Norway, Luxembourg, and Iceland. Each inhabitant still has, on average, more than €30,000 per year at his or her disposal.

The only country among the original EU-15 countries that has been virtually unable to increase its purchasing power over the long term is Greece. On the other hand, the Visegrad countries, the Baltic states, and Croatia are gradually working their way up, where disposable purchasing power has slowly but steadily risen in recent years

With a disposable purchasing power that, in some cases, is only a tenth of that of a Swiss citizen, the remaining states of the Western Balkans lag well behind. In terms of purchasing power, Romania and Bulgaria are also still quite weak compared to the rest of Europe.

Turkey’s purchasing power can only be determined for brief periods of time, with its current annual inflation rate at 80%. Moldova and Ukraine bring up the rear with respect to purchasing power, based on data taken at the end of 2021, before the Russian invasion. For ethical reasons, the values for Russia and Belarus are no longer shown.

What Can Be Expected When Forecasts Have Become Increasingly Unreliable?

Forecasting the growth of disposable purchasing power has become particularly difficult for the current year and will likely continue to be difficult in the years to come. The underlying calculations can no longer be based on the substantial data of an economy due to external factors such as the war in Europe, the pandemic, and the mood of certain political decision-makers. As a result of related factors, shifts in inflation and interest rates have occurred

Moreover, the reported figures, which have risen in nearly every country, are nominal values – that is, they include inflation. Consequently, that will ultimately result in the painful decline in real income for a substantial part of the population.

According to current GDP and inflation forecasts, Ireland, Latvia, and Iceland have the most favorable conditions for a nominal increase in individual purchasing power. The major European economies have slightly above-average prospects, while Spain, in relation to this outlook, shows certain alarming factors in terms of purchasing power forecasts.

Disastrous declines in purchasing power are expected in Ukraine and Turkey. In Ukraine, the decline may be much more severe depending on the course of the war. In Turkey, on the other hand, runaway inflation and a dramatic drop in the value of the national currency are expected to have a massive impact on private purchasing power.

Can Long-term Consequences Be Opportunities?

The world we live in is constantly changing, driven by a number of interconnecting factors at the local, regional, and international levels. We have recently seen global issues have a greater impact in even shorter periods of time. As a result, economic situations and consumer behavior have become more difficult to predict. Nevertheless, investors and developers need to make decisions regarding their retail locations, expansion plans, refurbishments, retail mix, and so on. These sometimes-unpredictable changes are what make economy-related issues exciting and human. The availability of time-sensitive data has never been more important, and insights from past and ongoing projects provide a higher level of security when it comes to decision making. Finally, we must ask ourselves how we can make progress and learn from such disruptions at the individual and collective levels. Resilience and flexibility have once again become important attributes of both real estate as well as for leaders.